.png)

Summary

This past week, markets were faced with a triple whammy of data: A Federal Reserve interest-rate hike (perhaps its last of this cycle), ongoing turmoil in the banking system, and a key jobs report for the month of April.

After raising interest rates by over 5.0% in a little over one year, the Fed may finally be considering a pause in its rate-hiking campaign. But the long and variable lags of the past year of interest-rate increases may already be upon us and impacting the real economy. This can be seen from the uncertainty in the regional-banking system and incremental tightening in lending standards, to a softening in manufacturing and the housing sector.

Although overall U.S. stock market volatility remained modest throughout the week, that wasn’t the case for the stocks of regional banks. A handful saw their stocks plunge by as much as 50% on Thursday, only to recover most of that ground on Friday as their shares rallied. In the wake of recent bank failures, regional banks’ balance sheets have come under intense scrutiny.

With roughly 85% of S&P 500 companies having reported first-quarter results as of Friday, key metrics this earnings season have come in better than their one-year averages, according to FactSet. In addition, the research firm reports that the overall earnings outlook for full-year 2023 has improved in recent weeks.

With the Fed and ECB week behind us, traders' attention now turns to US inflation data, key loan and trade figures from China and the Bank of England meeting.

The broader cryptocurrency market failed to chart any notable changes in the past seven days, with the total capitalization remaining more or less what it was back then. Bitcoin is trading more or less where it was exactly seven days ago, at $28000. The cryptocurrency plunged toward $27,500 in the middle of the week, but the bears were unable to sustain the selling pressure and the price recovered. The momentum is shaky, and market participants are on their toes as the cryptocurrency is trading within a range between $27,000 and $31000.

For those of you who haven’t been following the space recently, PEPE is a brand new memecoin minted less than three weeks ago. This brand new memecoin is now traded across all major exchanges, including Binance, and has managed to acquire a market cap of over a whopping $1 billion soaring a whopping 1200% in seven days.

Crypto exchange Binance closed withdrawals of Bitcoin for the third time in 12 hours due to an overflow of transactions on the network. Over the weekend, The Bitcoin network’s mempool (the memory pool of pending transactions waiting for validation from a node before being committed to a block on the blockchain) reached over 450,000. The congestion is believed to be due to the surge in what are known as BRC-20 transactions. These transactions launched in March of this year and are an experimental fungible token saved on the Bitcoin base chain.

Macro and news

FED & BCE

For its tenth meeting in a row, the U.S. Federal Reserve lifted its benchmark interest rate, but it hinted at the possibility of a pause in its rate-hiking cycle. As it raised its benchmark rate to a range of 5.00% to 5.25%, the Fed’s latest policy statement removed language that had been in previous statements indicating that it “anticipates that some additional policy firming may be appropriate.”

The Fed states that the next interest rate moves will depend on how the economy and inflation evolve, taking into account the lagged effect of the rate hikes already implemented, which means data-dependent pause. The Fed, which expects inflation moderation to be slow, considers it premature to talk about rate cuts. QT remains unchanged, with monthly balance sheet reductions of usd 60,000 mln in Treasuries and usd 35,000 mln in MBS.

While Chair Powell did not comment explicitly that the Federal Reserve was ready to pause interest rates, some of the language in the Fed statement hinted that a pause may be coming. The statement removed the phrase, "some additional policy firming may be appropriate," and replaced it with language that it would assess incoming data to determine "the extent to which" additional tightening would be appropriate.

Despite the ongoing turmoil in the regional banking system, Fed Chair Powell reiterated the message that the U.S. banking system is "sound and resilient." He also noted that the "conditions in the banking sector have broadly improved since early March," which seemed somewhat dated given the recent turmoil we have seen in regional banks like PacWest Bancorp.

Powell sees a growing tightening of credit conditions stemming from the problems in U.S. regional banking, which he does not quantify in terms of equivalent interest rate hikes, but which he expects to have an impact on economic activity, the labor market and inflation, although the impact is uncertain for the time being.

99.2% odds of rate cuts before the end of the year.

The European Central Bank (ECB) decided on Thursday to raise its interest rates by 25v bps, to 3.75%. With this new increase, it slows the pace at which it has been raising the price of money since it began this path in July 2022, in which there have been increases of 75 and 50 basis points. Thus, the ECB slows the pace of hikes, but marks differences with the US Federal Reserve, ensuring that "the ECB is not in a pause, this is clear," said the president of the institution, Christine Lagarde.

Although the ECB has lifted its foot off the accelerator, inflation continues to tighten. The CPI in April in the Eurozone stood at 7%, a slight rise that keeps the central bank on its toes. Although all indications are that prices should continue to moderate, the ECB will continue to tighten monetary policy to bring inflation to a sustainable and sustained level of 2% year-on-year.

Lagarde has stated that there are still large upside risks to inflation, especially from a number of recent wage settlements and high corporate profit margins, adding that financial conditions are not yet sufficiently tight.

US Jobs

Despite higher rates and uncertainty in the banking system, the labor market has been a source of strength in the U.S. economy. This past week's jobs data was no exception, as U.S. nonfarm payroll jobs increased by 253,000 in April, above consensus estimates of 185,000. But there were meaningful downward revisions to both the February and March figures, bringing the three-month average jobs gain to just 222,000. The unemployment rate came in at a healthy 3.4%, still near multi decade lows. Wage growth in the U.S. also remains elevated, at 4.4% year-over-year, still above the Fed's target range of 3.5% for wage gains.

However, we are already beginning to see a trend change in other readings of U.S. employment. US job openings declined sharply in the first quarter.

Not much soft-landing support in decline in job openings rate (blue), which is at 2y low, when it’s met with an uptick in layoff rate (orange), which is at highest since December 2020.

S&P 500 companies mentioning layoffs have grown the most since the Great Financial Crisis on a year-over-year basis.

Q1 Earnings

The estimated decline in first-quarter S&P 500 earnings has improved from last week and is now at just 0.7% year-over-year, Refinitiv data showed on Friday, thanks to another round of upbeat results from companies including Apple.

The first-quarter reporting period is in the final stretch, with results now in from 419 of the S&P 500 companies. About 77% of reports are beating analysts' earnings expectations. Also, in aggregate, companies are reporting earnings 7.2% above expectations, the highest "surprise rate" since the third quarter of 2021, according to Refinitiv.

The 0.7% projected decline compares with an estimated fall for the first quarter of 1.9% a week ago and a drop of 5.1% at the start of April. Despite the improved forecast, the first quarter still would mark a second straight quarterly fall for U.S. corporate earnings, or an "earnings recession," which last occurred when COVID-19 hit corporate results in 2020.

Apple q1 23 earnings

Eps $1.52, est. $1.43

Revenue $94.84b, est. $92.68

Apple to buy back up to added $90b in shares

Products rev. $73.93b, est. $71.91b

IPhone 51,334 vs 48,660 est (Iphone revenue sets march quarter record)

Services 20,907 vs 20,960 est

Wearables 8,757 vs 8,380 est

Mac 7,168 vs 7,783 est

Ipad 6,670vs 6,667 est

Apple Q1 revenues were down 2.5% year-over-year, 2nd straight quarter of negative YoY growth. Net income was down 3% vs. the same quarter last year.

Eurozone Macro Data

The latest batch of hard economic data for the German industry is a clear reminder to never count chickens before they are hatched. After a strong rebound in February, almost all hard data plunged in March. Risks of recession in Germany and thus in the Eurozone increase.

German Factory Orders (M/M) Mar: -10.7% (est -2.3%; prev 4.8%)

German Factory Orders WDA (Y/Y) Mar: -11.0% (est -3.1%; prev -5.7%)

German Retail Sales (M/M) March: -2.4% (est 0.4%; prev -0.4%)

German Retail Sales NSA (Y/Y) March: -8.6% (est -6.5%; prev -5.9%

Germany March (M/M) Industrial production: - 3.4%; est. -1.5%

Germany March (Y/Y) Industrial production: 1.8% ; est. +1.8%

Eurozone Mar Producer Prices -1.6% on Month; +5.9% on Year

Eurozone Mar Ex-Energy PPI +0.2% on Month; +8.0% on Year

Banking Crisis

The sudden collapse of Silicon Valley Bank and the subsequent failures of Signature and First Republic have focused attention on the US regional banking sector, as investors and policymakers looked for other lenders that might share the same vulnerabilities. The KBW regional banks index has dropped nearly 30 per cent since early March.

Despite the Fed's more optimistic take on the banking sector, regional banks in the U.S. continue to come under pressure. After First Republic Bank was acquired by J.P. Morgan last weekend, this past week additional West Coast-based regional banks, including PacWest Bancorp, Western Alliance, and Zions Bank, all saw substantial declines in their share prices, before rebounding somewhat on Friday.

PacWest, which is lower by over 70% year-to-date, has announced that it is seeking strategic alternatives, including a potential sale of its business, and will seek to maximize shareholder value. This comes even as PacWest highlighted that it has not experienced out of the ordinary deposit outflows and that its cash and liquidity position exceeds its uninsured deposits.

Shares of PacWest soared 38% in premarket trading Monday, adding to a near 82% pop on Friday. The company on late Friday evening announced a dividend cut to just 1 cent per share from 25 cents per share in the previous quarter. PacWest CEO Paul Taylor reassured investors that the bank’s businesses remain “fundamentally sound”.

Western Alliance shares pared losses after plummeting by nearly 60% following a Financial Times report that the lender was exploring strategic options, including a potential sale of all or part of its business. Western Alliance denied the FT report, calling it "categorically false in all respects," and said it was weighing legal options against the newspaper

U.S. Federal Reserve Chair Jerome Powell on Wednesday reiterated the banking system remains resilient despite strains in March, after the central bank delivered a 25-basis- point rate hike and signaled a pause in its tightening cycle. Powell also said bank deposits had stabilized.The following chart does not seem to be in sync with Powell's words.

Nonetheless, markets have been searching for "who is next" among regional banks, and we would expect further intervention and consolidation among the 4,100 commercial banks in the U.S. in the months ahead. Banking turmoil isn't over as regional lenders face risk of commercial property (CRE) credit losses. We recommend the reader to read our previous newsletters where we have dealt in detail with all the issues surrounding CRE.

Credit Crunch ?

It is time to keep a close eye on financial conditions, a significant tightening of bank lending standards often leads to a recession, and lending standards are tightening significantly. Seems that a credit crunch is looming, corporate credit crunch is just getting started.

A credit crunch could erode American consumers’ strength, which for over a year now has been a critical guardrail against a recession. Observers including former Treasury Secretary Larry Summers and JPMorgan Chase CEO Jamie Dimon have recently warned that inflation is wearing away the stockpile of savings many Americans accrued during the pandemic, increasing the chances of a recession.

There was already a trend toward tighter credit conditions, but the US regional Bank Crisis has made it even harder for small firms to get funded. Raises the odds of recession.

Last week, the New York Fed reported that financial conditions in its region had deteriorated sharply. The trouble is rekindling concern that a credit crunch is underway.

Crypto News

The White House is considering taxing Bitcoin miners in the U.S. for 30% of the electricity they use to offset the economic and environmental costs they impose on society, including the rising cost of electricity for households. The measure, proposed as part of the 2024 Budget, would apply to all miners under the name "Digital Asset Mining Energy (DAME) excise tax." The U.S. government believes that the mining industry, and implicitly cryptocurrencies, do not sufficiently benefit the community and do not generate the expected benefits. If approved, the tax could generate $3.5 billion in revenue over ten years and potentially cause a further exodus of miners to other less hostile countries.

Google Cloud is partnering with Polygon Labs to make it easier to build and deploy decentralized applications (dApps) on the Polygon blockchain (MATIC) and Polygon zkEVM. This partnership will help developers by providing resources, additional capital, and full control over the hosting of deployed nodes. The collaboration aims to increase transaction throughput for gaming, supply chain management, and decentralized finance (DeFi).

Mastercard rolls out new Web3 solutions. Mastercard introduced Mastercard Crypto Credential, a suite of solutions focused on identification and transparency in blockchain technology. One of the solutions replaces public addresses, which are a long series of numbers and letters, with an alias in the format "alias.mastercard". To deploy its infrastructure, Mastercard has partnered with players in the cryptocurrency ecosystem, such as Lirium, Mercado Bitcoin, Polygon Labs, Ava Labs, Aptos Labs and the Solana Foundation. The U.S.-based company notes that the technology aims to bring value to different areas such as NFTs, ticketing and payment solutions.

Bitcoin is experiencing an anomaly where a decline in active addresses is perversely aligning with increased network congestion. And now the ensuing volatility quakes seem to have hit Binance hard, with the world's largest crypto exchange recording its largest-ever Bitcoin outflow over the past few hours.

Binance closed withdrawals of Bitcoin for the third time in 12 hours due to an overflow of transactions on the network. Over the weekend, The Bitcoin network’s mempool (the memory pool of pending transactions waiting for validation from a node before being committed to a block on the blockchain) reached over 450,000. The congestion is believed to be due to the surge in what are known as BRC-20 transactions.

As a result, despite a fall in active addresses, the Bitcoin network congestion and the attendant fees only increased, leading many to conclude that the network was facing "inorganic" activity, which then gave rise to heightened DDoS attack fears.

The Bitcoin Ordinals Protocol recently made waves when it allowed for the creation of NFTs on the Bitcoin Network. Each Bitcoin can be subdivided into 100 million units called Satoshis (or Sats for short). The protocol allowed Bitcoin node operators to inscribe each Satoshi with data, including NFT enabling smart contracts. This then gave rise to the Ordinals, which are NFTs that can be minted directly onto the Bitcoin blockchain

The BRC-20 is an experimental token standard that allows for the creation of fungible tokens using the Bitcoin Ordinals Protocol, where inscriptions of JSON data are used to deploy token contracts as well as mint and transfer the tokens. Do note that BRC-20 tokens, unlike their ERC-20 counterparts in the Ethereum ecosystem, do not support smart contracts, thereby precluding much of the DeFi space from functions such as liquidity provision. Basically, the BRC-20 contract is etched onto the Satoshis and is not programmable, which means that it cannot automatically execute actions based on a prior set of conditions. On the other hand, since BRC-20 tokens can be minted and traded using Bitcoin wallets, they remain easily accessible to the crypto community.

This is a revenue boost for Miners, as the average fee paid per block has reached 2.905 $BTC, near past bull peaks.

Cryptos: spot, derivatives and “on chain” metrics

Bitcoin has not left the $27000 and $31000 price range for a month now. What we do perceive is a clear inability of demand to push upwards. The market is unable to consolidate above the Vwap anchored to the local highs of this value area, several attempts have already been made and a clear sellers' zone is beginning to be seen. However, the Vwap (green) is acting as a strong support. In the short term, the scenarios to plan are ambiguous and we limit ourselves to monitoring these two anchored Vwaps. Their breakout and consolidation will give us the key to the next move.

Bitcoin 02/05/23 10 min chart

Bitcoin 08/05/23 10 min chart

Bitcoin 02/05/23 4h chart

Bitcoin 08/05/23 4h chart

We continue to believe that a retracement move towards the upper part of the major range ($25000) coinciding with the Vwap anchored at the lows of the last major impulse would still fit within a bullish imbalance scenario and in fact would help to offload some of the leverage and Fomo present in the market. However, deeper retractions into the larger range could be very dangerous.

Leverage Ratio on Futures pushing up hard while aggregated Funding Rate dumping. Means, high leverage shorts on the table.

Bitcoin network activity is growing thanks to Taproot.

Bitcoin network activity is growing thanks to Taproot. Bitcoin is not just a P2P payment system anymore, it's an L1 blockchain like Ethereum. You can create basic smart contracts on the Bitcoin network. The recent increase in network activity is due to a spike in total daily transactions driven by Taproot addresses.

Classic markets

So far in 2023 we've had just 7 mega caps account for 90% of the gains in the S&P 500 year to date. These gains have led to Apple and Microsoft making up 13.4% of the index's market capitalization. That's the highest concentration in about 60 years!

NASDAQ has climbed to its highest since September 2022 but only 3% of members have made a new 6-month high.

S&P 500 is poised to have its smallest monthly trading range since 2017, which has triggered an almost unprecedented volatility crunch.

This phenomenon is forcing strategies that are controlling their exposure via volatility into the market and we are now hearing that also hedge fund clients are adding length again "on a FOMO thesis", according to Goldman Sachs. Numerous risk-based strategies like Vol-Control Funds, Risk Parity and CTAs have been increasing their equity exposure in this lower vol environment. This has led to a consistent underlying bid for stocks, further helping to dampen volatility.

The recent decline in volatility stems more from strategic equity positioning than any widespread economic optimism. The market more than ever is dominated by flows, flows that are “price agnostic” and do not even remotely attend to fundamental or macroeconomic criteria, however, they may have run out of ammunition.

From Goldman:

We estimate that total Systematic strategies purchased +$173.8B worth of global equity futures over the past 1-month. Total Systematic strategies have now downside asymmetric skew for Global Equities. Check out our estimates for an up big (+$25.2B to buy) vs. down big (-$276.3B to sell) tape over the next 1-month. In other words, the buyers are out of ammo.

The scenario proposed last week was fulfilled. However, it seems that the SPX is cornered between 4150 and 4050 points. We will follow these levels closely and wait for consolidations above these levels to raise scenarios. The market is not moving anywhere at the moment and short term flows derived from options are the ones that set the intraday moves. The market has not reacted positively to the last Fed meeting and this is an issue to be taken into account. Negative catalysts are the ones that can impact the market the most. The banking crisis continues and is far from over.

02/05/23 SP500 futures big picture

08/05/23 SP500 futures big picture

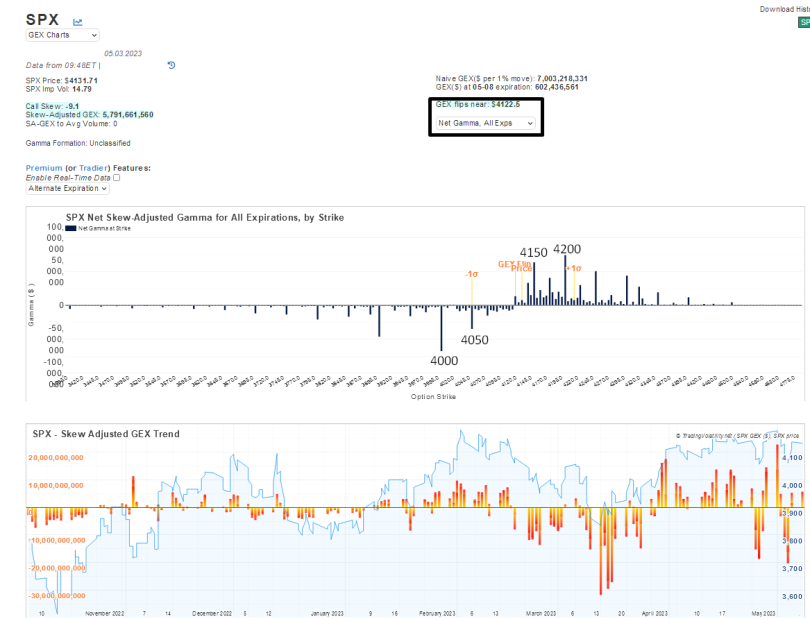

The 4150-4200 gamma call wall has been acting as resistance since the last OPEX. We have again registered a strong rejection in this area, as shown in the chart above and is presumed to be a very tough area to go through. Special attention to the put wall at 4050, last week it was tested and saved twice and with strong buying initiative. According to Goldman it is the trigger level for systematic selling.

Gamma Profile 01/05/22

Gamma Profile 08/05/22

Two weeks ago Net Gamma change was awesome, check last friday:

Net Gamma Change 02/05/22

Net Gamma Change 05/05/22

It is an aimless market that iIn the next few months, the market will confront the debt ceiling debate. Even without a U.S. default, the Treasury's rebuilding of the TGA signifies a reduction in liquidity rather than an increase. Additionally, COVID-related student loan forbearance is set to expire, employment retention credits will have worked their way through the system, and the percentage of U.S. adults with more credit card debt than savings has risen from 21% in 2021 to 36% in 2023.s continuously liquidating the over-positioning of one side and the other, in a game known as gamma squeeze.

.png)