.png)

Summary

We have a huge week ahead: Fed, ECB, Apple and April payrolls. At the May Federal Open Market Committee (FOMC) meeting on Wednesday, the Fed is widely discounted to raise another 25 basis points to 5.25%, the highest rate since 2007. In turn, at the ECB decision on Thursday, the market is also pricing in a 25 basis point rise in the deposit rate to 3.25%, although there is a possibility of a 50 basis point hike. However, watch out for the April payrolls report on Friday, which could surprise many with a sharp drop.

The busiest week of the Q1 earnings season is now in the history books and, contrary to widespread expectations of a plunge, several bumper earnings reports from megacaps helped push the SPX up to 4,200 points and keep Bitcoin in the $27000 - $31000 range.

The Federal Reserve’s policy pendulum has swung back to inflation fighting. Following a tense few weeks of having to stave off a potentially crippling financial crisis, policymakers have turned their attention back to battling stubborn inflation that threatens to send the economy into recession later this year. With the banking problems seemingly at bay for now, Fed officials have made it clear in recent remarks that tight monetary policy is likely to be around for a while, and a pivot is unlikely. However, we are of the opinion that the banking turmoil is far from over and that regional lenders face the risk of losses on commercial real estate loans.

Regulators seized troubled First Republic Bank early Monday, making it the second-largest bank failure in U.S. history, and promptly sold all of its deposits and most of its assets to JPMorgan Chase in a bid to end the turmoil that has raised questions about the health of the U.S. banking system. It’s the third midsize bank to fail in less than two months. The only larger bank failure in U.S. history was Washington Mutual, which collapsed at the height of the 2008 financial crisis and was also taken over by JPMorgan in a similar government-orchestrated deal.

Last week, the crypto industry was largely dominated by regulatory developments. Industry leaders continued to express concerns about the regulatory climate in the United States, with some firms contemplating migrating in response to the Securities and Exchange Commission’s (SEC) crackdown. In contrast, the European Union had more clarity, as the parliament approved proposals in the Markets in Crypto Assets (MiCA) bill.

Macro and news

Data released over the past month suggest that the economy is already slowing faster than expected. The economy’s slowdown reflects the impact of the Federal Reserve’s aggressive drive to tame inflation, with nine interest rate hikes over the past year. The surge in borrowing costs is expected to send the economy into a recession sometime this year.

The Commerce Department reported that America’s gross domestic product, adjusted for inflation, rose at a tepid 1.1 percent rate in the first quarter, lower than many economists had expected. The rate was down from the 2.6 percent rate in the last quarter of 2022. Reports last week also showed that the housing market shrank for the eighth consecutive quarter (U.S pending home sales (mom) (mar) actual: -5.2% vs 0.8% previous; est 0.5%) and investment by businesses in new equipment declined for the second quarter in a row.

On the inflation front, data out last week reported that consumer prices rose at an annual rate of 4.2 percent during the first quarter of 2023. The rate was higher than in the last quarter of 2022, and still well above the Fed’s two percent target.

GDP rose at a 1.1% annualized rate on the back of the strongest consumer spending in nearly two years. The Federal Reserve’s preferred underlying inflation metric accelerated to a one-year high. The 3.7% increase in consumer spending reflected gains in both goods and services, including a surge in purchases of motor vehicles. Business investment in equipment posted the biggest drop since the start of the pandemic and inventories subtracted the most from GDP in two years.

The economic slowdown is expected to be more evident in the second quarter, with economists forecasting GDP to grow at a stall-speed pace of 0.2%. While a recession isn’t assured, many economists, including those at the Fed, expect the cumulative effect of monetary tightening, a retrenchment in business investment, a slowdown in consumer spending and tightening credit conditions to ultimately tip the economy into a downturn.

Many indicators of economic and industrial activity are beginning to show a serious slowdown, with the exception of China.

Shipments of boxes plunge downward to below 2009 lows.

German retail sales fell more than expected in March, as consumers in Europe’s largest economy reined in their spending even before adjusting for higher inflation.

German Retail Sales (M/M) March: -2.4% (est 0.4%; prev -0.4%)

German Retail Sales Y/Y) March: -8.6% (est -6.5%; prev -5.9%)

US factory activity contracted for a sixth-straight month in April, the longest such stretch since 2009 and a sign of lingering malaise in manufacturing.

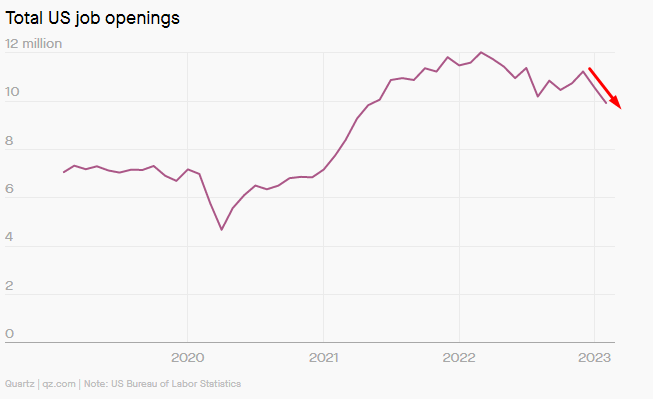

The US economy's demand for workers is finally waning.

The US saw the number of job openings fall by 632,000 in February, while the percentage of Americans in their prime working years participating in the labor force rose 0.4 percentage points. Those indicators suggest that the US labor market tightness of the past two years is beginning to ease as more people actively seek employment. That’s good news for efforts to battle inflation, but it also represents a weakening of workers’ negotiating power in the face of the Federal Reserve’s interest rate hikes.

This upward trend in jobless claims is a sign that the labor market has begun to react to the Federal Reserve’s tightening monetary policy meant to combat inflation, continuing claims are up 22.5% YoY

The Federal Reserve's recession probability model has reached the highest point since 1982.

There’s still a >90% chance the Fed announces another rate hike this week. The ECB on Thursday is likely to deliver a 50 bps hike unless bank lending surveys and loan growth data due on Tuesday change the picture dramatically.

Wednesday, the Fed returns to the debate. Either raise rates to tame inflation, but banks feel more pain.Or leave rates unchanged to support banks, but risk inflation spiking. At this point, there is no good solution, the work should have been done with head and sense much earlier.

This rapid rise in interest rates has not only created great stress in the financial sector, but interest payments on debt are skyrocketing. Higher for too long is not really sustainable.

Fed hiking cycles of this magnitude have historically always led to recessions. Since 1955, the Fed has never increased the Federal Funds Rate 400+ bps without a recession following.

Chile’s overall copper production is currently as low as it was 18 years ago, nearly down 10% from its recent peak. It is important to note that Chile holds a dominant position in the supply of this metal, accounting for nearly 30% of the total global production, akin to the OPEC of the copper market.

High-grade copper discoveries are becoming increasingly challenging as most deposits found in the last decade are characterized by having low-grade mineralization that would not be economically viable at the current metal prices. Additionally, the potential nationalization of Chile's lithium industry raises critical questions about the stability of the country's copper market, which could further complicate the global supply of this metal.

These factors are among the main reasons for such a compelling demand and supply case for copper in the long-term. The potential transition to a green economy relies on an ample and accessible supply of metals, which is unattainable today.

Debt ceiling

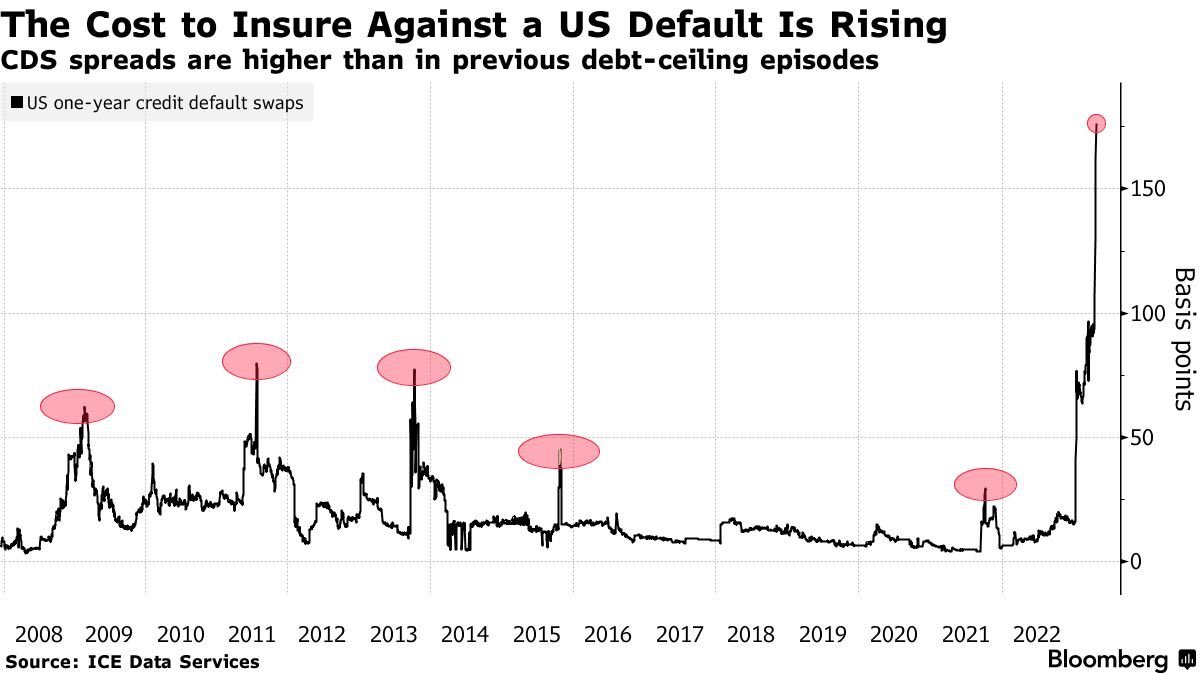

Treasury Secretary Yellen warns that the US will default by June 1st if the debt ceiling is not raised. Since January, the US Treasury has been taking “special accounting maneuvers” to avoid default. These special maneuvers will no longer help avoid default after this month. It is useful to remind the reader that the debt ceiling has been raised, extended or revised 78 times since 1960.

In this instance, House Republicans have demanded drastic spending cuts and a reversal of some aspects of President Biden's agenda, including his student loan forgiveness programme and green energy tax credits, in exchange for votes to raise the debt ceiling. This, in turn, has prompted objections from Democrats in the Senate and from President Biden, who said last week that the issue is "not negotiable".

The president, however, is coming under increasing pressure from business groups, including the US Chamber of Congress, to discuss Republican proposals. A default, which would be the first in US history, could upend global financial markets and shatter trust in the US as a global business partner.

Experts have warned that a default could also see the US head into a recession and lead to rising unemployment. It would also mean that the US would be unable to borrow money to pay the salaries of government employees and military personnel, social security checks or for other obligations, such as defense contractor payments.

The Treasury plans to increase borrowing through the end of the quarter ending in June, totalling about $726bn, about $449bn more than projected earlier this year. Officials have said this is partly due to lower-than-expected income tax receipts, higher government spending and a beginning-of-quarter cash balance that was lower than anticipated.

Cost of CDS Spreads to Insure Against US Bankruptcy:

- 2008: 60 basis points

- 2020: 10 basis points

- NOW: 175 basis points

The cost of CDS spreads are now 3x what it was in 2008 and 18x what it was during the pandemic.

Q1 Earnings

At the midpoint of the Q1 2023 earnings season, S&P 500 companies are recording their best performance relative to analyst expectations since Q4 2021. Both the number of companies reporting positive EPS surprises and the magnitude of these earnings surprises are above their 10-year averages. The index is reporting higher earnings for the first quarter today relative to the end of last week and relative to the end of the quarter. However, the index is still reporting a Y/Y decline in earnings for the second straight quarter.

Overall, 53% of the companies in the S&P 500 have reported actual results for Q1 2023 to date. Of these companies, 79% have reported actual EPS above estimates, which is above the 5-year average of 77% and above the 10-year average of 73%. In aggregate, companies are reporting earnings that are 6.9% above estimates, which is below the 5-year average of 8.4% but above the 10-year average of 6.4%.

Five of the eleven sectors are reporting year-over-year earnings growth, led by the Consumer Discretionary and Industrials sectors. On the other hand, six sectors are reporting a year-over-year decline in earnings, led by the Materials and Health Care sectors.

From last week's earnings we highlight:

VISA

Adj Eps $2.09, est. $1.99

Eps $2.03 vs. $1.70 y/y

Net rev. $8.0b, est. $7.79b

Cross-border volumes at constant currency +24%

Total visa processed transactions $50.1b, est. $49.78b.

MICROSOFT

Rev. $52.9b, est. $51.03b

Eps $2.45

Intelligent cloud rev. $22.08b, est. $21.89b

More personal computing rev. $13.26b, est. $12.15b

Productivity rev $17.52b, est. $17.1b

ALPHABET

Q1 Revenue $69.80 bln vs. estimate $68.946 bln

Q1 Eps $1.17 vs. estimate $1.07

Oper Income $17.42b, est. $16.19b

Google cloud Rev. $7.45b, est. $7.46b.

Youtube ads Rev. $6.69b, est. $6.65b.

Rev. ex-tac $58.07b, est. $56.98b

Google Other Rev. $7.41b, est. $7.22b

Other bets Revenue $288m, est. $299.9m

Google ad Revenue $54.55b, est. $53.79b

Authorized the company to buyback up to an additional $70b in shares of class a and c.

Alphabet may incur additional charges.

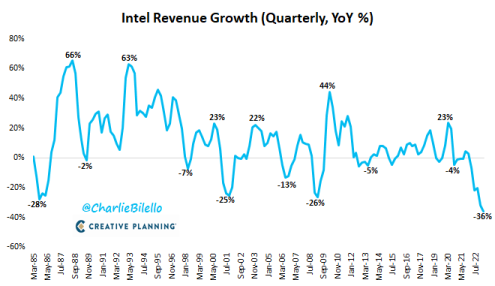

INTEL

Eps: $0.10, est. $0.20

Revenue $14.04 billion, est. $14.45 billion

Intel’s revenue declined 36% year over year in the quarter that ended Dec. 31. The largest YoY decline in company history.

The company recorded a $664 million net loss, compared with a profit of $4.62 billion in the year-ago quarter

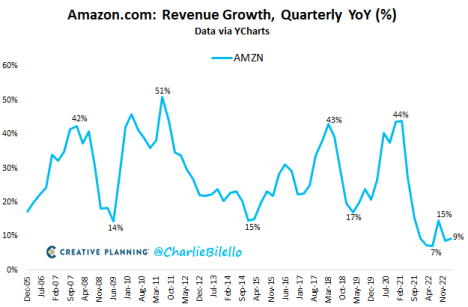

AMAZON

Eps $0.31, est. $0.21

Q1 Rev. $127.40b, est. $124.55b

The volatility in Amazon's share price during the presentation of results is unparalleled, we remind the reader that it is a company with a capitalization of more than 1 trillion dollars. Amazon turned negative after erasing gains of as much as 12% in the aftermarket. It seems that the Amazon web services guidance was not well received along with a worrying YoY revenue growth.

Banking Crisis

Regulators seized troubled First Republic Bank early Monday, making it the second-largest bank failure in U.S. history, and promptly sold all of its deposits and most of its assets to JPMorgan Chase in a bid to end the turmoil that has raised questions about the health of the U.S. banking system. JP Morgan will assume $92 billion of First Republic’s deposits, $173 billion in loans and $30 billion in securities, FDIC is covering $13 billion in losses.

It’s the third midsize bank to fail in less than two months. The only larger bank failure in U.S. history was Washington Mutual, which collapsed at the height of the 2008 financial crisis and was also taken over by JPMorgan in a similar government-orchestrated deal.

Jamie Dimon, JP Morgan´s CEO, said in a conference call with both reporters and investors that he believed “this part of this (banking) crisis is over.” Other midsize banks reported their results last week and the vast majority of them showed deposits had stabilized and profits remained relatively healthy. The outlier was First Republic. Turing Capital does not believe that this is the end of this financial crisis.

US regional banks have been at the center of the worst financial turmoil since the 2008 crisis. The small and mid-sized regional banks remain "an area of concern" because of their increased lending exposure to the commercial real-estate sector (CRE), which is grappling with high vacancy rates and may come under stress. Over the last 12 to 18 months, most of the bank lending that has occurred in America has come from US regionals and most of that lending has actually gone into commercial real estate.

Many experts have warned the US commercial real-estate sector (CRE) could face problems as high borrowing costs and tighter credit conditions following the recent banking turmoil complicate matters for big property owners as they seek to refinance loans. Nearly $450 billion in commercial real-estate debt is due to mature in 2023 , meaning a final payment on those loans are due.

Expected drawdowns in commercial property prices compared to the GFC. Morgan Stanley.

Fund managers see commercial real estate as the most likely source for a systemic credit event.

Since the onset of the pandemic, banks have ramped up their exposure to CRE sector debt. Regional banks’ share of financing into the CRE sector rose from 17% in 2017 to 27% in 2022, making it the largest source of funding for the sector.

We can highlight two interrelated concerns. The first is that regional banks may be saddled with bad debts should their real estate debtors default. The second is that the sector will be starved of capital as regional banks, already under stress, are unable to continue lending to the sector.

Small banks live off CRE cause they struggle with efficiency, economy of scale, & alternative product lines.

Loans from the Fed to the banking system saw higher demand versus as of Wednesday versus one week earlier. Discount window borrowing and the Bank Term Funding Program both saw week-over-week increases. Lending in the foreign repo facility fell to zero.

In the wake of SVB's collapse, the Fed implemented the BTFP, an additional facility to help banks improve their liquidity. First Republic Bank took $13.8bn from the BTFP & failed anyway. Why? The BTFP treats the symptom, not the disease. As long as deposits keep falling, bank stress will rise.

Remember, banks are leveraged organizations that only hold a fraction of customer deposits as liquid cash. Continued deposit withdrawals thus place ongoing pressure on a bank's liquidity and its business model. Furthermore, falling deposits not only create risks for the banks themselves, but given the leveraged nature of a fractional reserve, debt driven economy, it risks a wider economic bust.

With the Fed continuing with its QT (quantitative tightening), an ongoing stagnation in lending risks an even larger decline in the M2 money supply, creating further downside risks to economic growth. This is when banks will feel even more pressure, for as opposed to just liquidity concerns, a deteriorating economy adds to credit risk. In response to rising credit risk, banks will further tighten lending standards, risking an even larger decline in M2 and the economy, and so the cycle repeats.

Large banks will continue to pretend like they are “helping” the system. However, in reality, it seems that large banks don’t want this crisis to end. In March, HSBC bought SVB’s UK business for $1.They just reported quarterly pre-tax profit of nearly $13 billion, 49% above expectations. HSBC also announced a $2 billion stock buyback.

Total FDIC Losses by Bank:

1. Silicon Valley Bank: $20 billion

2. First Republic Bank: $13 billion

3. Signature Bank: $3 billion

On top of this, UBS convinced Swiss regulators to cover $10 billion in losses on Credit Suisse.

The strangest part about the regional banking crisis is that most people have no clue it’s happening. Three of the largest bank failures in history just occurred and it’s barely making headlines. People are so overwhelmed by inflation that nothing else matters and the authorities continue to cling to the discourse that nothing is happening here:

White House: will continue to monitor the situation in the banking system, this is not 2008, this is a very different time.

U.S. Treasury: U.S. banking system remains sound and resilient, Americans should feel confident in the safety of their deposits.

Mark Twain famously said: history never repeats itself but it often rhymes

Credit Crunch ?

It is time to keep a close eye on financial conditions, a significant tightening of bank lending standards often leads to a recession, and lending standards are tightening significantly. Seems that a credit crunch is looming, corporate credit crunch is just getting started.

A credit crunch could erode American consumers’ strength, which for over a year now has been a critical guardrail against a recession. Observers including former Treasury Secretary Larry Summers and JPMorgan Chase CEO Jamie Dimon have recently warned that inflation is wearing away the stockpile of savings many Americans accrued during the pandemic, increasing the chances of a recession.

There was already a trend toward tighter credit conditions, but the US regional Bank Crisis has made it even harder for small firms to get funded. Raises the odds of recession.

Crypto News

Last week, the crypto industry was largely dominated by regulatory developments. Industry leaders continued to express concerns about the regulatory climate in the United States, with some firms contemplating migrating in response to the Securities and Exchange Commission’s (SEC) crackdown. In contrast, the European Union had more clarity, as the parliament approved proposals in the Markets in Crypto Assets (MiCA) bill.

On April 17, the SEC declared its readiness to regulate decentralized finance (DeFi), which critics say would slow down or impede the sphere’s growth. SEC chairperson Gary Gensler confirmed that DeFi would not be exempt from their supervision. They plan to modify the definition of “exchange” to include decentralized platforms such as DEXs.

Reports from April 16 revealed that the SEC served crypto exchange Bittrex a Wells Notice, alleging that it breached regulations by not registering as a broker-dealer, clearinghouse, or exchange. On April 17, the SEC charged Bittrex “for failing to register as a national securities exchange.” The exchange criticized the SEC’s action, noting that it always complied with the law and is keen to clear its name in court. The company also criticized the move as part of a more comprehensive campaign to stamp out cryptocurrency from the United States.

SEC Chairman Gary Gensler appeared at an oversight hearing before Congress, where many questions related to the FTX bankruptcy were discussed at length. During the oversight hearing, committee chairman Patrick McHenry asked whether Ethereum (ETH) is a security or a commodity. Gensler was non-committal in his response, stating that particular crypto tokens should be evaluated based on the Howey test. Gensler appeared to have dodged several questions during the oversight hearing, exemplifying the extensive case of regulatory unclarity.

With regulatory ambiguity in the United States, domestic companies are turning their attention overseas for investment prospects. In particular, Coinbase is reportedly considering the UK as a “hub of web3 innovation.” At the same time Coinbase also disclosed that it had procured an operating license in Bermuda and is planning to establish an offshore derivatives exchange there.

On April 20, the EU Parliament adopted both the proposal for a regulation on markets in crypto-assets (MiCA), and the proposal for a regulation on information accompanying transfers of funds and certain crypto-assets for tracing transfers of crypto-assets.

MiCA will:

- Create a harmonized framework for the crypto assets not currently covered by the existing EU and Luxembourg legal framework.

- Replace existing national frameworks and establish uniform rules for crypto-assets at EU level.

- Establish uniform requirements for transparency and disclosure in relation to issuance, operation, organization and governance of crypto-asset service providers.

- Establish consumer protection rules and measures to prevent market abuse, and the regulation is limited in scope to the crypto-assets that do not qualify as financial instruments, deposits or structured deposits under EU financial services legislation.

- Set out the terms and definitions of the referenced crypto-assets

EU Member States shall designate the national competent authorities. The Accompanying Regulation will ensure that the so-called “travel rule”, already used in traditional finance, will in future cover transfers of crypto assets so that information on the source of the asset and its beneficiary will have to “travel” with the transaction and be stored on both sides of the transfer.

The majority of MiCA's provisions shall apply from 18 months after the date of its entry into force as well as the Accompanying Regulation. However, crypto asset transfer service providers in scope will have to adopt a phasing plan no more than nine months after its entry into force.

Google will offer support for the deployment of Polygon nodes within its Google Cloud. Polygon is a well-known Layer 2 platform for Ethereum, which enables the development of decentralized applications (dApps), offering increased scalability, speed and low cost.

The goal is to enable developers using Google solutions to create and deploy their applications on Polygon. In this way, they will be able to access the Polygon network nodes and enjoy all its advantages in just a few minutes.

The alliance will also benefit the Polygon ecosystem in general, as it will increase the availability and diversity of nodes in the network, which translates into greater security, performance and decentralization. It will also drive innovation and growth of Polygon-based dApps, especially those that make use of zero-knowledge (ZK) technology, which enable faster and cheaper transactions.

Google Cloud has long been demonstrating its interest in the Web3 development business. That is, the blockchain-based decentralized web. The partnership with Polygon Labs positions Google Cloud as a leading provider of cloud solutions for developers who want to create the future of the web.

Visa, the global payment giant, is expanding its crypto division with new software engineer hires. The company has posted several job openings for senior software engineers who can help it develop and launch new products based on public blockchain networks and stablecoin payments. According to Cuy Sheffield, the head of crypto at Visa, the company has an "ambitious crypto product roadmap" that aims to drive mainstream adoption of crypto technology.

Visa has been actively involved in the crypto space, partnering with various platforms and providers to enable crypto payments and services. The company has also expressed interest in StarkNet, a layer 2 blockchain built on Ethereum, which could facilitate easier bill payments for self-custodial wallet users. Visa's crypto hiring spree shows its commitment to its crypto strategy and its vision for the future of payments.

The global movement towards de-dollarization is picking up. Last week in New Delhi, Russian Deputy Chairman of the State Duma Alexander Babakov suggested that Russia and India could launch a common currency and even include China in the initiative. Brazilian media suggested that the common currency could be a BRICS-wide effort, implying additional participation from Brazil and South Africa. The bloc could launch its own currency as a way of shifting away from the dollar’s dominance.

Cryptos: spot, derivatives and “on chain” metrics

Bitcoin posted its biggest weekly loss in five months last week. However, framing the movement within the structures and value areas, nothing alarming has occurred. What we do perceive is a clear inability to consistently exceed the $29,000 - $31,000 zone. Interesting details are extracted from this short term chart: the market has failed to consolidate above the Vwap anchored at local highs and the Vwap anchored at the relevant lows of the range. In this situation, we believe that a second attempt at bearish imbalance is most likely to occur.

Bitcoin 24/04/23

Bitcoin 02/05/23

We continue to believe that a retracement move towards the upper part of the major range ($25000) coinciding with the Vwap anchored at the lows of the last major impulse would still fit within a bullish imbalance scenario and in fact would help to offload some of the leverage and Fomo present in the market. However, deeper retractions into the larger range could be very dangerous.

Classic markets

Bank of America's fund manager survey shows how most investors seem to be hiding in big tech stocks as a ''safe haven'' equity trade and nobody wants to be long US Dollar anymore. It seems that the long tech trade is starting to become very crowded. Could we stop saying hedge funds are massively short now? They're net long.

So far in 2023 we've had just 7 mega caps account for 90% of the gains in the S&P 500 year to date. These gains have led to Apple and Microsoft making up 13.4% of the index's market capitalization. That's the highest concentration in about 60 years!

NASDAQ has climbed to its highest since September 2022 but only 3% of members have made a new 6-month high.

S&P 500 is poised to have its smallest monthly trading range since 2017, which has triggered an almost unprecedented volatility crunch.

This phenomenon is forcing strategies that are controlling their exposure via volatility into the market and we are now hearing that also hedge fund clients are adding length again "on a FOMO thesis", according to Goldman Sachs. Numerous risk-based strategies like Vol-Control Funds, Risk Parity and CTAs have been increasing their equity exposure in this lower vol environment. This has led to a consistent underlying bid for stocks, further helping to dampen volatility.

The recent decline in volatility stems more from strategic equity positioning than any widespread economic optimism. The market more than ever is dominated by flows, flows that are “price agnostic” and do not even remotely attend to fundamental or macroeconomic criteria.

At the same time, liquidity in the global system is once again dwindling following recent interventions by the authorities to alleviate the banking crisis. The following chart compares the SPY with global liquidity and Wresbal (Reserve Balances with Federal Reserve Banks).

24/04/23 SP500 futures big picture

02/05/23 SP500 futures big picture

Two bullish days wiped out in 2 hours. This is what happens when the market is dominated by dumb flows with everyone systematically biased to the upside chasing the price and the flows. The positive GEX two days ago was ridiculously wild. The 4175-4200 gamma call wall has been acting as resistance since the last OPEX. We have again registered a strong rejection in this area, as shown in the chart above.

Although we expect pullbacks towards the GEX flip level (4130), reentry into the range is ugly and negates any bullish scenario in this upper value area. If we lose the anchored Vwap that has served as support during the month of April and the market consistently enters into a negative gamma regime, curves may follow.

Gamma Profile 01/05/22

Net Gamma change today is awesome.

.png)