.png)

Resumen

Once again we are facing an intense week in terms of very sensitive data for the market. As we already know, the market currently lives on the same wavelength as the FED, taking the US CPI data with a whole match ball that repeats itself every month. For the first time since November 2022, the market no longer expects any interest rate cuts in 2023. Just two weeks ago, markets were expecting 2 rate cuts in 2023. Currently, banks expect CPI to be between 5.8% and 6.7%, with a median of 6.2%. If inflation comes in at 5.8%, it would mark its 7th consecutive monthly decline. If inflation stands at 6.7%, it would mark its 1st rise since July 2022. Huge range with record highs of uncertainty, ready for another high intensity week?

Macro and news

Relevant data for this week:

Many macroeconomic indicators point to an imminent drop in inflation, especially on the goods side; however, the services and wages variables are the big unknowns and the ones that may stifle expectations of a disinflation process that Powell has reiterated is already underway.

Last week we learned about important data in Germany and the Eurozone:

Germany dec. industrial production falls 3.9% y/y (largest decline since march 2022); est. -1.6%

Germany dec. industrial production falls 3.1% m/m (largest decline since march 2022); est. -0.8%

German CPI (Y/Y) Jan: 8.7% (est 8.9%; prev 8.6%)

- German CPI (M/M) Jan: 1.0% (est 0.8%; prev -0.8%)

- German CPI EU Harmonised (Y/Y) Jan: 9.2% (est 10.0%; prev 9.6%)

- German CPI EU Harmonised (M/M) Jan: 0.5% (est 1.2%; prev -1.2%)

Eurozone consumers ended 2022 on a low, with retail sales collapsing by 2.7%. Real retail sales are down 2.8% from a year ago.

Powell and the market insist on discounting a scenario of disinflation and soft landing / mild recession, however some metrics and indicators make us remain extremely cautious about this discounted scenario.

The 2-10s U.S. yield curve is now the most inverted since the early 1980

Individuals are with their savings at minimums, according to the following charts, it seems that loans and cards have financed the expenses. We are beginning to see restrictive financial conditions from the banks..

Banks tightened their lending standards to historical extremes. In the past, default waves followed within 6-12 months.

Powell last week was speaking on TV in an informal and certainly even humorous interview. Here are the headlines:

- The message from last week's fomc was that the disinflationary process has begun, but there is still a long way to go.

- Probably need to do further interest-rate increases. We will respond to the data.

- Jobs report certainly stronger than anyone expected

- If data were to continue to come in stronger than expect, would certainly raise rates more

- If data continues to come in stronger than expected, the Fed will raise rates accordingly.

- It will be a couple of years before the Fed's balance-sheet decline comes to an end.

- The United States is only at the beginning of the deflationary process.

- Housing disinflation has not yet occurred, but I expect it to occur in the second half of this year.

- It is possible that this cycle may be different, the labor market remains strong while wages are moderating.

As usual with Powell, ambiguity in his statements. A dovish tone tentatively celebrating a start of disinflation but cautious ahead of upcoming data. The market needs a dovish Powell and waning inflation data to keep the hope of a pivot alive and to keep the recent rally from turning into a bear market rally. This week again a life and death matchball with the US CPI monthly data.

Cryptos: spot, derivatives and “on chain” metrics

The crypto ecosystem, despite having experienced a historic January in terms of rises, continues to navigate the storm initiated by FTX, this time the spotlight is on the regulator. These are the main news of the past week.

- Binance to suspend USD bank transfers

- Paxos to stop issuing dollar-pegged Binance token BUSD

- Sec to sue Paxos for listing BInance USD stablecoin

- Kraken is under investigation by the US SEC

- Kraken agreed to shutter US crypto-staking operations

- Gemini, Genesis reach $100M agreement over Earn program

- DCG sells shares in Grayscale as it seeks to raise funds

- Revolut launches crypto staking for UK and EEA customers

- Tether (unaudited stablecoin) reports $700 million Q4 net profit in latest report

In sum, banks taking deposits from crypto clients, issuing stablecoins, engaging in crypto custody, or seeking to hold crypto as principal have faced nothing short of an onslaught from regulators in recent weeks. Time and again, using the expression “safety and soundness,” they’ve made it clear that for a bank, touching public blockchains in any way is considered unacceptably risky. While neither the Fed/ FDIC/ OCC statement — nor the NEC statement a few weeks later — explicitly ban banks from servicing crypto clients, the writing is on the wall, and the investigations into Silvergate are a strong deterrent to any bank considering aligning itself with crypto.

So why the push by bank regulators now? The FTX collapse and its ensuing effects, particularly on Silvergate, provides much of the answer. Financial regulators weren’t interested in FTX while the fraud was underway (with the exception of the SEC and its chairman Gensler, who had oddly close ties to the organization), but ever since the exchange failed in spectacular fashion, they are now contemplating ways to avoid the next such collapse. FTX as an offshore exchange was not directly supervised by financial regulators (aside from FTX US, which was a marginal stub), so it was outside of their direct aegis. However, regulators believe that they might have a silver bullet in the fiat on- and off-ramps on which the industry relies. If they can choke off fiat access, they can marginalize the industry — on and offshore — without regulating it directly. Do not worry, from Turing Capital we will be very attentive to the evolution of events, we insist once again that a regulatory clarification is positive for the long term.

Bitcoin 06/02/23

Bitcoin 13/02/23

The market after the explosive upward move in January is pulling back and testing the value area. It is now where demand must really show that it is in control. Buyers must support the price above the value area, we are certainly at a key moment.

In the short term and looking closely at the order book, we note that the 21400 zone is being defended, so be careful with the loss of this level.

Analyzing Binance perpetual futures we clearly observe a loss of buying momentum via delta and some selling entry. The $21000-21500 area should be defended by buyers.

The skew, which measures the difference between the IV (implied volatility) of OTM puts and the IV of OTM calls is moving away from the buying and greed climax zone, the market seems to be starting to demand puts and selling calls.

skew 06/02/23

skew 13/02/23

The time structure of the volatility curve clearly reflects the nervousness of the market in general in the face of the U.S. inflation data, a strong short-term spike in the curve.

06/02/23

13/02//23

Bitcoin options market gamma profile on deribit

$21750 as the strike with the highest notional gamma in view of the important inflation data.

Peak in the GEX and sharp decline in the GEX is usually an indication of underlying weakness. We are very careful that the market does not enter into a negative gamma regime, as this could alter the market dynamics.

Classic markets

The SPX is trying to effectively unbalance the entire core value area to the upside, however a high GEX and a prominent gamma call wall between 4150-4200 points is preventing it from making progress. This week of highly sensitive data for the market will allow us to know the final outcome of this scenario.

A bullish imbalance failure and a consolidated break below 4100-4080 (gamma flip) could trigger heavy selling. The stock market seems to want to go to the sidelines, however since last week, we have seen strong divergences with the fixed income markets, which have experienced notable stress. At the same time, we have started to see strong call activity on the VIX, with a notable pointing of the VVIX (VIX volatility).

Goldman "CTAs have purchased ~$120bn of global stocks in the last month across the 21 indices GS stratsmonitor, almost all are in the 100th percentile for length". Pretty stretched and climatic

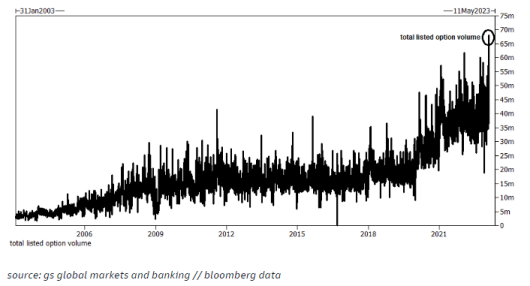

Two trends that are a bit concerning and both happening at the same time.

1) Record options volume, the highest ever

2) Record retail participation as a % of total market volume

.png)