.png)

Summary

Has the recession already begun? Will the Fed succeed in bringing down inflation without causing an economic “hard landing”? How much more will the interest rates rise and how long will they stay inflated? How much will earnings contract and how many more outlook cuts will be needed? No one knows for sure, not even Jerome Powell.

U.S. equity markets finished broadly higher this past week after a critical slate of inflation data provided further evidence of a definitive cool-down in inflationary pressures, which again revived "soft-landing" hopes.

While volatility in equity markets declined to the lowest levels in over a year this week, volatility across fixed-income markets remained elevated this week, with benchmark interest rates ultimately ending the week near the highest-levels since the Silicon Valley Bank collapse in early March.

Earnings season shifts into full gear next week, with some of the world’s largest companies set to report earnings, including Johnson & Johnson, Bank of America, Netflix, Lockheed Martin, Tesla, Morgan Stanley, IBM, American Express, and Procter & Gamble, among many others. The latest updates on the housing market will become available, including March housing starts, building permits, and existing home sales. We’ll also get inflation readings from the U.K., eurozone, and Japan, as well as first-quarter GDP figures from China.

The crypto market closes one of its best weeks of 2023. Most assets experienced a significant surge in value following positive events in the industry. As a result, the market capitalization increased by over $100 billion and, at one point, had topped the $1.3 trillion mark.

Bitcoin is flying high on the back of an 8% value boost that took it past the $30,000 resistance level. The king of cryptocurrencies is back above $30k for the first time in 10 months. It is an impressive and somewhat surprising achievement for an asset that had finished last year at nearly half the value.

Ethereum successfully completed the Shanghai (Shapella) upgrade on Wednesday, allowing validators to unlock their staked ETH and their rewards accrued so far and freeing up a staggering $34 billion ETH in the process. The event helped it increase considerably in value and took it past the much coveted $2,000 level.

Macro and news

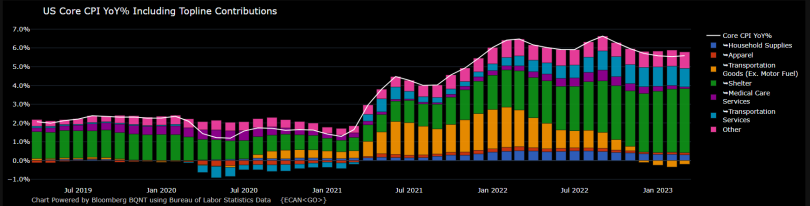

A key measure of consumer prices dropped sharply in March, suggesting that high U.S. inflation is beginning to wane. The Labor Department reported the Consumer Price Index (CPI) rose at an annual rate of 5% in March, its lowest level since 2021. This was down from a 6% year-over-year gain in February and below the 5.3% gain economists were expecting. The CPI reading is the latest indicator that inflation is trending steadily downward after hitting 40-year highs in 2022.

Core CPI, which excludes both food and energy price increases, is considered to be a better indicator of the price growth ahead. Core CPI grew by 0.4% last month, in line with estimates.

In its March policy statement, the FOMC said “some additional policy firming may be appropriate.” However, the March CPI number likely increases the chances the FOMC will seriously consider pausing its rate hikes at its upcoming meeting on May 2-3.

According to CME Group, markets are currently pricing in a 72.9% chance of another 25 bps rate hike this month, which would bring the target fed funds rate to between 5% and 5.25%. The market is also pricing in an 83.3% change the Fed will cut its target range back below its current level by the end of the year.

US March inflation

Headline CPI yoy: 5% (vs 5.1%)

Headline CPI mom: 0.1% (vs 0.2%)

Core CPI yoy: 5.6% (vs 5.6%)

Core CPI mom: 0.4% (vs 04%)

Shelter remains the main contributor in the Core CPI, despite a softening in MoM data.

The US inflation rate has reached the same level as the Fed funds rate of 5 percent, but the central bank is not yet comfortable with a pause.

The market continues to discount sharp interest rate declines throughout the second half of this year and 2024. The market does not believe the Fed.

Inflation adjusted wages are down for a record 24th consecutive month. That's 92% of Biden's entire presidency

U.S. PPI

U.S. PPI (mom) (mar) actual: -0.5% vs -0.1% previous; est 0.0%

U.S. PPI (yoy) (mar) actual: 2.7% vs 4.6% previous; est 3.0%

U.S. Core PPI (mom) (mar) actual: -0.1% vs 0.0% previous; est 0.2%

U.S. Core PPIi (yoy) (mar) actual: 3.4% vs 4.4% previous; est 3.4%

Eurozone Macro data

Eurozone industrial production mom feb actual: 1.5% vs 0.7% previous; est 1.0%

Eurozone industrial production yoy feb actual: 2.0% vs 0.9% previous; est 1.9%

Eurozone retail sales mom feb actual: -0.8% vs 0.3% previous; est -0.8%

Eurozone retail sales yoy feb actual: -3.0% vs -2.3% previous; est -3.5%

Banking Crisis

Fallout from the U.S. banking crisis is likely to tilt the economy into a mild recession later this year, according to Federal Reserve documents released Wednesday.

Minutes from the March meeting of the Federal Open Market Committee included a presentation from staff members on potential repercussions from the failure of Silicon Valley Bank and other tumult in the financial sector that began in early March. Several policymakers questioned whether to hold rates steady as they watched to see how the crisis unfolded. However, they relented and agreed to vote for another rate hike “because of elevated inflation, the strength of the recent economic data, and their commitment to bring inflation down to the Committee’s 2 percent longer-run goal.

The banking system is showing signs of stabilizing after the collapses of Silicon Valley Bank (SVB) and Signature Bank, but the looming battle to stave off a national default could complicate that rebound. Congress has anywhere between June and the start of fall to raise the debt limit, which caps how much money the Treasury can owe to cover the nation’s bills, or risk a federal default, an outcome economists say could yield devastating effects for the economy. Treasury Secretary Janet Yellen told lawmakers after the collapses of SVB and Signature that a breach of the debt limit would be “completely devastating” to the banking industry.

JP Morgan CEO Jamie Dimon said in his annual letter to shareholders, the deeper turmoil “is not yet over” and “there will be repercussions from it for years to come”.

Most Wall Street banks are likely to report lower quarterly earnings and face a dour outlook for the rest of the year, with last month's regional banking crisis and a slowing economy expected to hurt profitability. Earnings per share for the six biggest U.S. banks are expected to be down about 10% from a year earlier. Banks start reporting results on April 14.

A lending slowdown may have begun only weeks after the failures of Silicon Valley Bank and Signature last month sent ripples through the financial system, according to another recent survey, by the Federal Reserve Bank of Dallas, published last week. The survey of 71 financial institutions, conducted between March 21 and 29, found that lending has already plunged.

There was already a trend toward tighter credit conditions, but the US regional Bank Crisis has made it even harder for small firms to get funded. Raises the odds of recession.

Obtaining credit has become more difficult for US consumers compared to a year ago.

US small businesses are feeling the credit crunch.

Lending standards never get this tight without a recession, according to Bank of America. The tightening followed the recent banking crisis, as lenders work to improve their risk management in the face of rising rates, exiting deposits, and increasing risk of non-payment.

We're seeing financial stress on the rise to levels that are similar to the LTCM collapse and Dot Com bubble bust.

The major issue in the wake of the banking crisis was whether regional and local U.S. banks would start cutting back on lending, which could accelerate the country’s spiral into a recession, as these institutions account for almost 40% of all lending.

A credit crunch could erode American consumers’ strength, which for over a year now has been a critical guardrail against a recession. Observers including former Treasury Secretary Larry Summers and JPMorgan Chase CEO Jamie Dimon have recently warned that inflation is wearing away the stockpile of savings many Americans accrued during the pandemic, increasing the chances of a recession.

The economy was able to survive tightening lending standards over the past year, although the credit crunch may deal a heavier blow, with firms like small businesses likely to struggle more than most. As for consumers, it will likely be a few months before the extent of damage begins to manifest in spending data.

Within the property industry, the US office market (CRE) is experiencing the most challenging operating conditions as high and rising vacancy rates are expected to result in significant downward pressure on rental income and valuations. Hence, combined with rising finance costs, there is a strong possibility of a significant number of loan covenant breaches and outright defaults. Approximately US $700 billion of mortgages (13% of total) are estimated to mature in 2023, with office being the largest sector expiring this year.

An example of the problem surrounding the office vacancy rate can be found in San Francisco. The ratio reaches historical levels with parabolic increases since 2020, no doubt covid and work from home have caused a change in the trend.

It is important not to underestimate the risks of contagion if a rapid loss of depositor confidence, or the operational challenges facing the US office market negatively impact lenders' appetite to finance the broader commercial real estate sector. Clearly the US office market remains a risk to investors and lenders.

Crypto News

This week saw the total cryptocurrency market capitalization soar above $1.3 trillion on the back of major increases from many coins. The sentiment has also improved considerably across the board. Bitcoin and Ethereum, the two largest digital currencies, have been making headlines lately as their values continue to rise. It recently crossed the $30,000 mark, while Ethereum, the second largest cryptocurrency globally, reached a multi-month high of $2,000.

Ethereum (ETH) has experienced an increase in value following the successful execution of the Shanghai and Capella (Shapela) upgrades. This bullish sentiment has propelled the price of Ether to reach a one-year high of $2,123 on April 14. The Ethereum decentralized finance (DeFi) ecosystem has experienced a 30% increase in daily fees as a result of the update, which has led to deflationary Ethereum Proof of Stake (PoS) token economics. This has resulted in a 32% increase in revenue in the last 24 hours.

Despite some withdrawals from the Ethereum ecosystem, there has been an uptick in Ether staking deposits, which shows a positive sign for the future of Ethereum. Furthermore, the reduction in the difference between the average staking price and the current Ether price means that the majority of the Ethereum ecosystem could soon be profitable.

US Stablecoin Framework Draft Bill Released: Potential Impact on the Crypto Industry

A new draft bill providing a framework for stablecoins in the United States was published in the House of Representatives document repository a few days before a scheduled hearing on the topic on April 19. The draft puts the Federal Reserve in charge of non-bank stablecoin issuers, such as crypto firms Tether and Circle.

According to the document, insured depository institutions seeking to issue stablecoins would fall under the appropriate federal banking agency supervision, while non-bank institutions would be subject to Federal Reserve oversight. Failure to register could result in up to five years in prison and a fine of $1 million. Issuers out of the United States would have to seek registration to do business in the country.

Among the factors for approval is the ability of the applicant to maintain reserves backing the stablecoins with U.S. dollars or Federal Reserve notes, Treasury bills with a maturity of 90 days or less, repurchase agreements with a maturity of seven days or less backed by Treasury bills with a maturity of 90 days or less, and central bank reserve deposits.

Turing Capital believes that a regulatory clarification in this opaque area of stablecoins is tremendously beneficial. The establishment of a regulation that clarifies and narrows down the requirements of stablecoin issuers is of vital importance for true institutional entry into the crypto ecosystem.

Developments coming on the FTX front. Attorneys and bankruptcy have been able to recover some $7.3 billion from the company’s assets. What is more, it was also revealed that a potential restart of the exchange is also being considered.

Twitter partners with eToro to enable users access to financial instruments. One of the world’s largest social media platforms, Twitter, has partnered with the popular retail-oriented financial app eToro. The goal of the partnership is to enable users to buy and sell stocks, crypto, and other financial assets.

London Stock Exchange taps digital trading platform to launch bitcoin futures, options trading. The goal is to start delivering the country’s first regulated trading clearing in bitcoin index futures and options derivatives

Cryptos: spot, derivatives and “on chain” metrics

Bitcoin has been stuck in the $26500 and $29000 range for almost 4 weeks and with clearly decreasing volume. Last week this range has been broken to the upside but leaving a price action that looks more like a short-term market top. Clearly the buyer control zone in this upper lower value area is $28,000. As long as the price remains above this level, the market is long.

Bitcoin 10/04/23

Bitcoin 17/04/23

Even breaks of the $28000 level and downward corrections to the VAH (value area high) of the main structure marked in gray could be framed within a normal process of upward imbalance of this main value area. The anchored VWAP marked in the previous chart, in case of deep retractions, would clearly be the level to watch.

Looking at ultra short-term charts, we observe a certain exhaustion of demand and supply entry with reversals characteristic of a market top. The anchored VWAP from highs is acting as clear resistance and the anchored VWAP at lows has recently been lost. We expect this structure to attempt a bearish imbalance based on the price action present in this value area.

Market and on chains metrics:

Digital asset investment products saw inflows totalling $114m last week, which is seeing continued improving sentiment for the asset class. This 4-week run of inflows now total $345m.

The Bitcoin market price remains above the average cost of production.

The spot vs. derivatives trading volume ratio shows the predominance of the derivatives flow throughout this rise. We believe that any organic movement must be accompanied by activity in the spot market.

As we can see in the chart below, the strong upward impulses have been accompanied by strong buying in the derivatives markets. Approaching the $30000 level we start to see strong selling, which could be position closures but should not be ignored.

Historically, BTC has shown a negative correlation with the Chicago Fed National Financial Index (NFCI), which is a gauge of financial conditions in the U.S. Rising NFCI typically indicates declining liquidity and leverage along with higher volatility and risk premia. Thus, BTC tends to rise when financial conditions ease and fall when they tighten. However, despite the significant tightening of financial conditions, BTC has weathered the banking turmoil well, rising by over 44% since the collapse of SVB on March 10.

Classic markets

We certainly expected more volatility ahead of the market's favorite data, US CPI and US PPI. Last week we suggested corrections or sidewaysness ahead of these data. In our opinion, the market has not taken the opportunity to break the 4150-4175 area and is starting to show signs of some buying exhaustion after a few weeks of complacency due to the remission of the banking crisis tensions. The earnings season is starting and it is to be expected that the market will rotate from ultra-short-term dynamics dominated by ODTE options to a more fundamental and medium-term positioning.

10/04/23 SP500 futures big picture

17/04/23 SP500 futures big picture

We expect market pullbacks this week although we are aware that the anchored VWAP marked on the chart is acting as clear market support.

The 4150-4175 gamma call has been acting as resistance since the last OPEX and the expiration of the JPM collar trade. The current high GEX (gamma exposure) in the market is a clear impediment to the market's upward progress. In a positive gamma regime market makers hedge against the market trend. In this case, selling pressure increases as the 4150-4175 gamma call is approached, preventing the market from moving higher.

These GEX levels, as we observed in the previous chart, have represented market tops in the short-medium term. When the bus is so full, it is impossible to keep going up the hill.

The crunch to implied volatility over the last 3 weeks is quite remarkable. As we observe, a fall in implied volatility in this market dynamic implies a rise in the index. However, this level of complacency becomes a risk in itself as we approach an event as important as the Q1 earnings. There is no riskier situation than when there is no perceived risk.

.png)