.png)

Summary

All risk markets, without exception, continue to celebrate in anticipation of a Fed Pivot and a "softlanding-mild recession" scenario with days of real "panic buying". It is next February 1st where the Fed will once again ratify for the umpteenth time whether the market is wrong or not. This week of transition before the Fed, we will know earnings of large companies and sensitive inflation data in the USA (PCE).

The current market mentality and its euphoria can be summarized in these 3 points:

- Better than expected economic data, we can avoid a recession.

- Worse-than-expected economic data, Fed to cut rates and the pivot will arrive.

- Economic data expected, soft landing possible.

After a disastrous 2022, markets and their participants want the market to go up and thus the narratives, which seem to be all aligned in the same direction: up. Is it irrational "fomo" or the real start of a new bull market? Reality (with the Fed's permission) as always will have the last word.

Macro and news

Relevant data for this week:

China closed all week for New Year and Fed members' blackout.

Tuesday: S&P Global Manufacturing PMI Flash (JAN). Microsoft and J&J results

Wednesday: Tesla, Boeing, AT&T results

Thursday: Durable Goods Orders MoM (DEC), GDP Growth Rate QoQ Adv (Q4) Intel and Visa results.

Friday: PCE Price Index YoY (DEC), Core PCE Price Index YoY (DEC)

In such a complicated macro environment and with crazed optimism festering in all markets, it is our duty to calmly assess whether such euphoria is in line with reality or pure wishful thinking.

The fixed income market is not discounting a recession. In a recession, the Fed cuts well below neutral (~2.5%) with credit spreads exploding. As of today, from what the market is discounting, the Fed will not cut below 2.75% and credit spreads will remain stable. This is a perfect and idyllic "disinflation" scenario. Curious to say the least, however, some data does not seem to be along those lines.

January New York Fed Empire Index at -32.9, Est. -8.6.

Industrial production is down more than 90 % since its peak last April 2021. The December reading was 1.65%.

New lows for the US Leading indicator. This indicator has a 100% success rate in anticipating recessions with a lag of 7-8 months. All indications are that the recession will begin in the second quarter and will be on par with the 2001 recession.

Last week's US retail sales data was one of the worst two-month declines since the GFC and the Covid confinements.

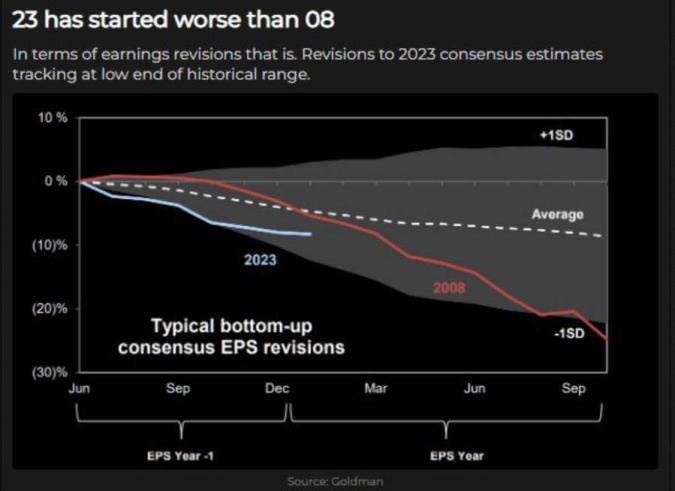

Historically, stock prices bottom between 6 and 9 months before EPS bottoms out as multiples begin to rise, reflecting Fed cuts and monetary policy ahead.

Earnings season is starting and it seems that the consensus expectations are going to be much higher than the actual data. Earnings are likely to be the first reality check the markets will face at the start of the year.

Morgan Stanley's Michael Wilson warns of big impact on eps

"Our work shows further erosion in earnings, with the gap between our model and forward estimates wider than ever. The last two times our model was well below consensus, the S&P 500 fell 34% and 49%.

In the first 3 weeks of 2022, we have already seen 56,000 people laid off in the technology sector. During 2022, we saw a total of 158,000 people laid off in the technology sector. It seems that the trend of layoffs that we started the year with is strong and assessing since October, we see almost twice as many layoffs in the tech sector than in 2001.

- Google: 12,000 employees

- Microsoft: 10,000 employees

- Amazon: 8,000 employees

- Salesforce: 8,000 employees

Recall, in turn, that the unemployment rate always reaches lows before a recession along with an inverted yield curve. We are right at this point at this very moment.

We have seen over the past two weeks how inflation in the US seems to be holding up, with some components experiencing declines, however this trend is not seen in services inflation. This component is 60% of US GDP and weights 75% in the CPI calculation.

Not to mention the new inflationary pressures that will be imported by the reopening in China and that some commodities are starting to give clear clues.

Looking at all these data, we draw the following conclusions:

- Despite the biggest job cuts in decades, stocks rise.

- Despite inflation remaining historically high, stocks are rising.

- Despite clear signs of a recession, stocks continue to rise.

For the first time in history, it seems clear that the markets want a recession, but a mild recession led by the Fed, which has repeatedly demonstrated its negligence in monetary policy by directly causing an inflationary explosion not seen in decades, which for some moments has been insisting on labeling it as transitory.

The Fed should be very attentive to the recent exuberance in the markets that has caused a severe easing of financial conditions back to February levels, nothing good in its fight against inflation, we do not rule out any surprises at the next Fed meeting.

The cycle of markets: financial conditions ease → stocks rise → commodity prices rise→ Inflation expectations rise→ rates rise→ dollar strengthens→ financial conditions tighten→ stocks fall→ commodities fall→ inflation expectations drop→ financial conditions ease.

To put things in perspective, the start of the year has been one of the best on record for the stock markets. The EuroStoxx has recorded the best start to the year since the index was created in 1987. Does this year's start hold up or is this euphoria the latest phase in a larger process of capitulation? it seems we will soon find out.

At the moment it seems that retail is "all in" with certainly climatic readings together with an institutional that again has a high exposure to risky assets similar to April, August and December last year. Will this time be the good one, ratifying what the market is discounting or will it be the fourth failed attempt of the market to start a bull market?

Call positioning in stocks such as Tesla is at one of the highest levels in the last two years.

At Turing Capital we believe that the long-awaited central bank pivot will come and merge with an economic recession and falling corporate margins caused by a systemic liquidity crisis. We are far from this point yet.

Cryptos: Spot, derivatives and on Chain metrics.

Within the current state of euphoria prevailing in the markets, in this newsletter we would like to point out the important latent risks on the market, which come directly from the contagion derived from the FTX-Alameda bankruptcy.

Over this weekend Binance has informed its retail customer base of a deposit service disruption that could halt incoming and outgoing bank payment transfers. The service disruption will affect US dollar bank account users wishing to buy or sell cryptocurrencies under USD 100,000 via the SWIFT payment system. The disruption will take effect on February 1. Similarly, Crypto.com appears to have discontinued its SEPA deposit and withdrawal service.

We believe that behind all this, there is growing regulatory pressure that is affecting crypto-friendly banks such as Signature Bank.

Signature Bank is a commercial bank headquartered in New York. At the end of 2021, it had assets of more than $118 billion and deposits of $85 billion. Previously, the bank had been known for its close relationship with the crypto ecosystem; by September 2022, digital assets accounted for nearly 25% of total deposits. Following the collapse of FTX, Signature Bank appears to be making efforts to put some distance from the cypto ecosystem. CEO Joe DePaolo has stated that the bank should be seen as more than just a cryptobank, The bank has been hit hard with the collapse of FTX, in fact its shares have fallen from $200 in August to $130 today.

Signature has its own digital payments platform called Signet. As shown below, there are many important names that use signature

CEO John DePaolo has communicated in the latest earnings call that the bank is reducing its concentration in Signet, most likely due to increasing pressure from the US banking regulator and the SEC.

Last year's prolonged crypto winter has hit some of the industry's largest firms hard. Silvergate, the digital asset-focused bank, reported that it lost USD $1 billion during the fourth quarter of 2022. The cryptoriendly bank had already previewed the red numbers earlier in January, in a presentation in which it warned that it had seen outflows of USD$8 billion during the fourth quarter.The company pointed to the bearish scenario in the crypto market, as well as the shakeout caused by the implosion of the FTX exchange and other high-profile firms as the main causes. An official statement read as follows:

"During the fourth quarter of 2022, the digital asset industry experienced a transformative shift, with significant over-leveraging in the industry leading to several high-profile bankruptcies. This dynamic created a crisis of confidence across the ecosystem and led many industry participants to shift to a 'risk averse' stance on digital asset trading platforms"

It is important to note that Silvergate Bank does not deal in cryptocurrencies: its clients buy and sell them on crypto exchanges that have accounts with this bank, and while the delivery of the cryptos themselves is done through the crypto exchanges, payment is done through deposits and withdrawals of traditional currencies to accounts opened within Silvergate Bank itself, through SEN, 24/7.

The deposits received by this bank are used to invest in traditional securities for its own account, mainly in those issued by the U.S. government, or to make loans to other customers; just like any other bank. The only new product launched by this bank (besides the SEN service) was the granting of credit lines guaranteed by Bitcoin, a product it called "SEN Leverage".

Although Silvergate Bank has stated that it has sufficient liquidity, and that it did not make loans to FTX (although it did receive deposits from it), last December several US Senators began to investigate the role of this bank in the FTX bankruptcy: they allege that it may have facilitated the transfer of funds from FTX's own clients to Alameda Research through SEN. The worst news so far came last January 11, when it was published that the Federal Home Loan Bank of San Francisco (an institution slightly similar to the IPAB, created to protect bank deposits) granted Silvergate Bank a loan for US$4.3 billion to increase its liquidity. The risks of a bank failure of Silvergate are very high and with a great possible impact on the crypto ecosystem.

The Genesis-Gemini-DCG soap opera continues. Last Friday, Genesis filed for bankruptcy after freezing withdrawals shortly after the collapse of FTX. In turn, a firm with which they were associated, Gemini, has threatened to sue them almost in tandem with announcing a 10% cut in its workforce. Days before, the U.S. Securities and Exchange Commission (SEC) had reported the company, which had a similar operation to Celsius, another of the big fallers in this "cryptowinter". It should be recalled that this firm is part of Digital Currency Group (DCG), which in turn also owns Grayscale and CoinDesk, the media that brought to light the embarrassments of FTX, and whose future is now an unknown.

Genesis now claims to have more than $150 million in cash on hand, liquidity that it hopes will help it as it faces the restructuring process. The firm is a subsidiary of Digital Currency Group, the cryptoasset conglomerate founded by Barry Silbert in 2015.

"While we have made significant progress in refining our business plans to remedy the liquidity issues caused by the recent extraordinary challenges in our industry, including the default of Three Arrows Capital and the bankruptcy of FTX, a judicial restructuring presents the most effective path to preserve assets and create the best possible outcome for all Genesis stakeholders," Derar Islim, interim CEO of Genesis, said via statement.

At Turing Capital, we will closely follow the evolution of all these events due to their possible high impact. An increasing regulatory pressure should not be interpreted as negative, to a certain extent, we consider that a regulatory clarification is necessary to allow massive institutional entry and to definitively purge all the "bad actors" that remain in the ecosystem.

On the technical side, the upward momentum is starting to give climatic signals, we are looking for corrections that validate this movement and represent a real change of character within this main value area.

Analyzing on-chain metrics in depth, we observe that this recent vigorous momentum is led by derivatives, we want to see organic growth hand in hand with the spot to believe in a real change in sentiment.

This divergence of the CVD (cumulative delta volume) of perpetual futures and spot makes us extremely cautious about the recent move. Much of the move has been fueled by short liquidations in a low liquidity environment. Shorts settlements did not come close to the amount settled on January 13 during the move above $20,000, however, during the past week the amount of short settlements is greater than what occurred during November and December of last year.

It is worth noting that the institutional whale activity has completely reversed its dynamics as shown in the following chart

Upward movements in Bitcoin have always presented a high correlation with the increase in total amount supply of stablecoins in circulation. This time this has not been the case, which could mean that the move has been driven by internal capital and as we have shown above by derivatives. We believe this needs to change in order to have a sustainable and healthy continuation.

The skew, which measures the difference between the IV (implied volatility) of OTM puts and the IV of OTM calls, is still in the buying climax zone, surpassing previous floor levels, which have led to a change in trend.

skew 16/01/23

skew 16/01/23

The time structure of the volatility curve at the money again shows a severe tightening in the short part belonging to the closest maturities. The market is discounting volatility for this week and next (FED).

Classic markets

SP500 Futures 01/16/23

SP500 Futures 01/24/23

We are facing an erratic market context that continues to be fueled by a rally in low quality assets. Once again, there is a clear market anxiety and "FOMO" (Fear of missing out) before the important FED meeting. The market is once again getting ahead of itself in a scenario of total uncertainty.

After the refusal to consolidate above 3960-4000, the market experienced last week a major correction that was quickly neutralized coinciding with the volatility of OPEX. We continue to insist that the big battle to be won by buyers is the conquest of 3960-4000, however the market shows signs of being once again overtaken in total greed mode. The market is not "trading" information, it is "trading" the "fear of missing out". Will all this "panic buying" be sustainable with what the FED has to say, the publication of earnings and the macroeconomic reality, it certainly seems very complicated to us.

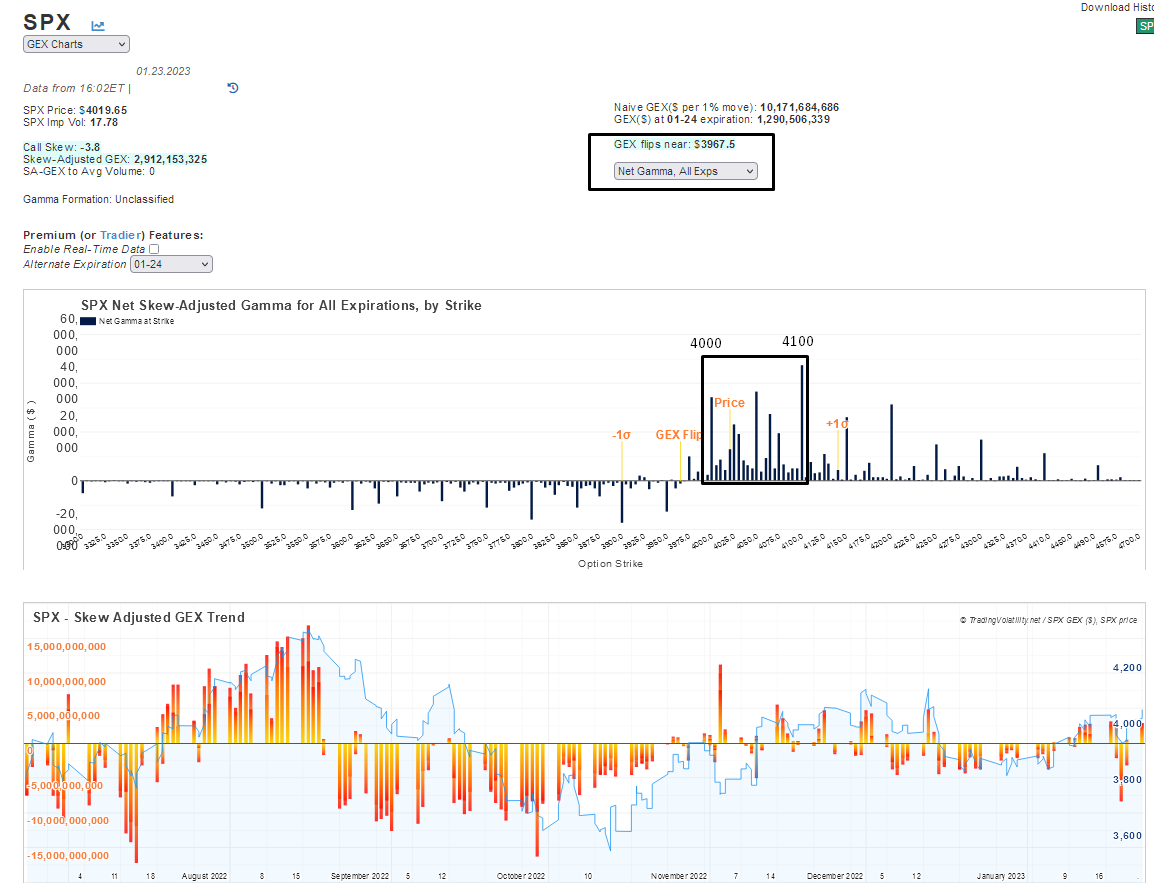

We continue to stress the dangerous dynamics in which the market is involved with ODTE (zero day to expiration) options on the rise since the middle of last year. 0DTE options on the SPX account for over 50% of all options traded on the index on a daily basis. That creates an environment where every day there is the opportunity for hundreds of billions of premiums to change hands to drive the market in either direction.

The constant change in market sentiment is reflected in a changing gamma profile practically from one day to the next.

On 01/18/23 the gamma profile showed the following structure, all the puts were burned

On 01/20/23, the opposite was the case, all calls burned and again a massive influx of puts.

To start this week after OPEX with all puts burned again with massive increase in open interest on the call side.

Such severe sentiment changes in a matter of a few hours are a clear sign that the market is in a phase that is driven more by emotions and long-short squeezes than by an organically functioning and healthy market.

It seems that the upside ahead of the important Fed event is limited to the 4000-4100 zone. As we have repeated on several occasions, the market is once again overextended.

.png)