.png)

Summary

Last week was perhaps the biggest week of the year. Powell and in turn Lagarde have delivered a severe blow to the table, nipping in the bud any expectations of a central bank pivot. The message has been clear, inflation remains "sticky" and central banks are going to continue to be aggressive in fighting it. We live in historic and unique times, central banks raising rates in recession. Markets have experienced a painful week with violent moves, the short term bullish pivot narrative has died overnight and Opex has exerted its powerful influence. A strong end to the year in line with 2022

Macro and news

Relevant data for this week:

Wednesday: US Consumer confidence

Thursday: US GDP Q3 final, US unemployment

Friday: US PCE November

In previous newsletters we have addressed various macroeconomic issues, earnings, employment, real estate, energy sector and economic activity indicators, this time we will focus on the clear and resounding message that central banks have given us during the past week. These are the most important points:

FED'S POWELL: we anticipate that ongoing hikes will be necessary to become sufficiently restrictive

FED'S POWELL: we still have work to do

FED'S POWELL: we require significantly more evidence of lower inflation

FED'S POWELL: we have not yet reached a sufficiently restrictive policy stance

FED'S POWELL: I can't promise that we won't raise our peak rate estimate at a future meeting

FED'S POWELL: we will make a decision in February based on financial and economic conditions

FED'S POWELL: If the data is bad, the peak could move up, but it could also move down if the

inflation data is weak.

FED'S POWELL: after moving so quickly, we believe it is appropriate to slow the pace of rate hikes.

FED'S POWELL: China faces a very difficult situation when it comes to reopening. it is hard to say how end of zero covid policy in China will affect us inflation

FED'S POWELL: there are no rate cuts in sep in 2023

FED'S POWELL: I don't see us considering rate cuts until we are confident that inflation is declining in a sustained manner

FED'S POWELL: we have a long way to go before returning to price stability

FED'S POWELL: in my opinion and that of my colleagues, we will have to maintain policy at a restrictive level for an extended period of time

The message, as we have said before, is clear, the Fed considers that it has a lot of work ahead to claim victory, they need more evidence that inflationary pressures are abating. It clearly states that there will be no rate cuts in 2023 and opens the door to the possibility of keeping rates high for a longer period of time than the market was discounting. This ultra hawkish tone has undoubtedly caught the market off guard and was reflected in the Fed fund rate forward curve.

Certainly and to be honest, the fed's pivot narrative of the past few weeks was underpinned more by wishful thinking and prayers than anything else. The complicated macro outlook ahead for 2023 and the deep pain experienced by the markets this year have prompted an anxious search for a revival that would give some respite to general sentiment, yet macro is moving at a very different speed to what the market normally demands.

On the ECB's side, Ms. Lagarde is nothing more than a bad and ill-timed replica of the Fed. Sometimes it gives the feeling that the "coach" is already merely a narrator, who narrates and reacts reactively rather than proactively. These are the main points to be highlighted by the ECB:

ECB`s new growth projections: now see the economy growing by 3.4% in 2022, 0.5% in 2023, 1.9% in 2024 and 1.8% in 2025

ECB: the Ecb's future policy rate decisions will be data-dependent and made meeting by meeting

ECB: according to eurostat's flash estimate, inflation in november was 10.0%, slightly lower than the 10.6% recorded in october

ECB: the Ecb decided to raise interest rates today and expects them to rise significantly further because inflation remains far too high and is expected to remain above target for an extraordinarily long period of time.

ECB: food price inflation and underlying price pressures throughout the economy have increased and will continue for some time

ECB: we now expect average inflation to reach 8.4% in 2022 before falling to 6.3% in 2023, with inflation expected to fall significantly over the course of the year

ECB: inflation is expected to average 3.4% in 2024 and 2.3% in 2025.

ECB: the governing council judges that interest rates will still have to rise significantly at a steady pace to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target

ECB'S PRESIDENT LAGARDE: the primary inflation risk is on the upside

ECB'S PRESIDENT LAGARDE: anyone thinking ecb is pivoting is wrong

ECB: from the beginning of march 2023 onwards, the asset purchase programme (app) portfolio will decline at a measured and predictable pace, as the eurosystem will not reinvest all of the principal payments from maturing securities

ECB: the monthly average decline will be €15 billion until the end of the second quarter of 2023, with the subsequent rate determined over time

Certainly, and making use of short-term memory, it is fascinating how Ms. Lagarde's discourse has changed in a few months from "transitory" and under control to practically catastrophic. In this situation, it is very difficult not to wonder whether the plane is going without a pilot.

In an important development, the ECB has given more details on the reduction of its monstrous balance sheet. We are all aware of the beautiful love affair between central bank balance sheets and financial markets, especially risky ones.

Realistically, the Fed after reducing its balance sheet (QT) and raising 375 basis points in a record period of time has achieved nothing. Inflation for 2021 was 7.0% and for 2022 it is 7.1%, this is a failure no matter how you look at it.

Although the market euphorically celebrated last Wednesday's slightly lower-than-expected inflation data, the reality is that inflation remains high and steady both in Europe and across the pond.

Big drops in airfares and used cars (-3% and -9% respectively) but in the items where the Fed is really paying attention there is no respite.

Central banks, with their reactive rather than proactive stance, are ultimately responsible for what we are experiencing. Now, in the end game, they are faced with the difficult choice of either fighting inflation and sending us straight into recession or allowing inflation to run wild but with less stress on the financial and credit markets. It seems that they have deliberately decided to calm inflationary pressures on the demand side, cooling economies and promising us a "soft landing". In our opinion this will not happen, even if they keep repeating the opposite.

ECB: according to latest eurosystem staff projections, a recession would be relatively short-lived and shallow.

FED'S POWELL: I don't believe sep qualify as forecasting a recession but the economy will have very slow growth

We continue to insist that the market has not even remotely discounted the profound political changes that will take place during 2022, which directly affect the functioning of the system as it is configured today and the structural energy problem, where Ukraine is not the cause but the fuse that has ignited all the dynamite that has been in place for a long time. The lack of capex in the classic fossil mining and extraction sector is a problem that has been dragging on for many years.

At Turing Capital, we believe that the Fed will slow the pace of rate hikes in order to keep rates high and constant for a longer period of time than the market expects. This pace of rate hikes is dangerous and can put the financial sector and citizens in serious trouble. The Fed is aware of this, or should be.

The U.S. public is at record lows in personal savings and the use of credit and credit cards is intensifying. Mortgage rates have jumped from 2.5% earlier in the year to as high as 7%. All of these issues have a high credit event risk for the financial sector.

From the Asian giant, we have seen how the Beijing government has come to the rescue of its sovereign bond market, injecting liquidity again. The economic activity figures, as we have already indicated in previous newsletters, do not invite optimism.

Crypto: spot, derivatives and on Chain metrics

This time, yes, big market moves last week. The market tried to anticipate the inflation data and Powell's speech, experiencing notable rises, which have been quite close to the ideas proposed last week. However, this type of movements, prior to a relevant event/news for the market, must be treated with great caution, the vast majority of the time they are completely reversed, as has been the case.

Bitcoin

12/12/2022

20/12/22

The market after shaking the relevant previous highs at $18,200 found a strong sell initiative that made it return abruptly and very vertically to the composite's vpoc of $17,000. The cumulative (green) steep slope structure effectively unbalanced but did not find continuation beyond the $18,000 level. The volume profile tools give us very clear information, they do not let it go out of either of the two extremes, the vah and val (value area high and value area low). After this brief bullish breakout we can say that the market has returned to the value, to its equilibrium zone where most of the trading of recent weeks is concentrated, highlighting the strong rejection of the original vpoc of $16600.

We are waiting for a clear operational event to show who has control over this area of value. They don't let it out at the top but they grab it when it falls, patience. Any bullish scenario must go through the recovery and consolidation of the $17000, as shown in this dynamic.

Any bearish scenario requires a break and consolidation below the vpoc of the 16600S.

The order book is still strongly protected at the bottom, with no relevant changes at the top, where there is hardly any resistance until $18500

The skew, which measures the difference between the IV (implied volatility) of OTM puts and the IV of OTM calls, once again reflects stressed markets. A week full of high-impact data for the market has once again pointed to the skew, fear is back in the market.

skew 12/12/22

skew 20/12/22

The volatility curve at the money returns to normal contango after last week's remarkable backwardation.

ATM IV 12/12/22

ATM IV 20/12/22

On December 30, we face the last important expiration of the year in Bitcoin options on Deribit (centralized exchange that gathers most of the volume traded in options). The "max pain" (level where most options end up with no intrinsic value, i.e. worth zero) is above $19,000. Undoubtedly, market makers are the first ones interested in the price reaching that level for this great expiration.

It is worth noting that this past Monday, 12/20/22, and once the complicated past week full of highly sensitive data and events for the market was over, there was an inflow of bullish flow in options, with large lots in bull call spreads and very OTM bull diagonal spreads.

In terms of delta (market aggression) on Binance perpetual futures, the recent downward movement does not seem to be accompanied by strong selling pressure on the market, it seems that demand has cushioned the impact, absorbing the selling. The weekly candlestick has a very ugly overlay in terms of price action, however in terms of delta the reading brings us a divergence.

The selling panic that resulted from the FTX event gave us insane numbers in terms of shorts paying for longs. Prior to the inflation data and last week's FED day the market was certainly starting to be overextended, which was reflected in the funding and Binance perpetual futures net longs.

We continue to observe outflows of Bitcoins from exchanges, such dynamics can be considered as moderately bullish under normal conditions, but in the middle of a CEX crisis these readings should be taken with a grain of salt. The shadow of the FTX and Alameda bankruptcy is very long and we are still immersed in the contagion effect.

Ethereum

Despite last week's declines, the market remains in balance within this lower value area marked in white and finding support at the $1200 vpoc.

12/12/22

We indicated that a support above the vpoc was the necessary condition to look for the top of the range and even to look for the imbalance of the structure, however when testing the relevant previous high, just like bitcoin, the supply found enough selling initiative. We remain nuetral until we identify a clear operating event within this minor value area.

20/12/22

Classic markets

The market after touching the gamma call wall of 4100, leaving a failure of bullish imbalance on it, has traveled the entire value area with a lot of verticality, this in the Wyckoff methodology is known as "sow" (sign of weakness). Last week we were at the edge of the precipice, however in this area the market began a strong bullish rally towards the upper part of the range in anticipation of the inflation data, which although it was better than expected, could be described as catastrophic. Minutes after the inflation data and with the spot market already open, the market plummeted, "buy the rumor, sell the news" by the book. From then on, Powell and Opex would do the rest.

SP500 Futures 12/12/22

SP500 Futures 12/20/22

Once again, we again have an operational weakness event in this value area, UT (upthrust), ST (secondary test), SOW (sign of weakness). The market remains in a very weak situation after last week's events and a bearish imbalance of the upper structure is the most likely scenario. We are looking for the classic break and test for bearish continuation, although we expect a gamma short squeeze to release all this misplaced bearish positioning with sudden last minute rushes after sending the Fed pivot narrative into a tailspin.

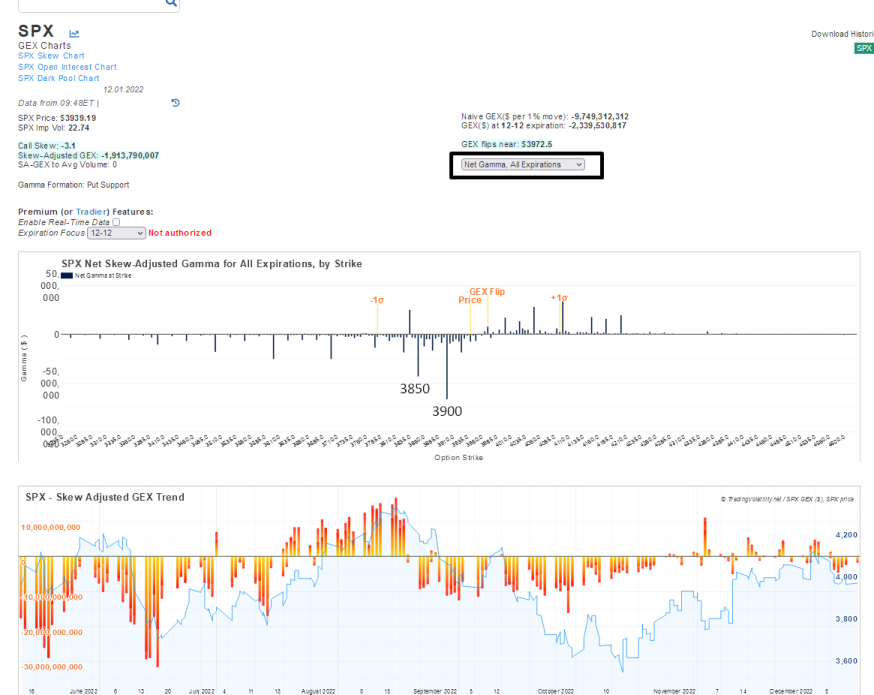

Gamma profile 12/12/22

December option expiration (OPEX) has exerted its powerful influence, it always does. The gamma profile of the market already marked the 3850-3900 zone as the area to close in the face of this massive derivatives expiration.

Gamma profile 20/12/22

This is the profile of the SPY for today, fear returns to the market, surely the market will clean up these late shorts to continue its way to lower highs. The market certainly looks like a video game in this final stretch of the year, where the game is to liquidate longs and shorts that are over positioned in a tremendously emotional and impulsive manner in our view.

.png)