.png)

Summary

The big storm in the crypto ecosystem came at the hands of Alameda Research and FTX. It took only 5 days to see this giant fall and cause a contagion effect that is being baptized as the "Lehman Brothers" of cryptos.

The bearish positioning readings in panic mode have reached climax levels, we will delve deeper into this issue throughout this newsletter.

The other relevant event of the week to note is the US CPI data, which came in below expectations, down 0.3%, resulting in a final figure of 7.7%. The market, eager for news and positive catalysts received it like a godsend, the SPY and the QQQ (An ETF that tracks the Nasdaq 100) experienced rises in the week certainly impressive in the case of the QQQ close to 10%. This week these gains will have to be validated by a battery of very sensitive macroeconomic data for the market (US PPI, housing and unemployment, Euro CPI-GDP), results of US companies related to the consumer and retail sector and OPEX (options expiration) on Friday.

Macro Analysis

Relevant data for this week:

- Tuesday: Industrial production China, GDP Eurozone, PPI USA

- Wednesday: UK CPI, US retail sales and NAHB housing index

- Thursday: Euro CPI, US unemployment, FED Philadelphia Manufacturing Index

- Friday: second-hand home sales USA

Also a busy week for the Fed and the ECB with a number of appearances

Last week's star of the week was undoubtedly the annual USA CPI for October, 7.7%, three tenths of a percent below expectations. The market exploded with jubilation at the data, thirsty for news and positive catalysts, no matter how small. However, at Turing Capital we treat this data with great caution. Delving into the CPI items, the positive surprise was due to a periodic adjustment in health insurance and used car prices.

On the other hand, inflationary pressures in Germany are continuing

The market anxiously looks for the PIVOT and clings to a 0.3% improvement to dream of a loosening of the Fed's Hawkish stance leaving a week for the history books in terms of moves across the financial asset space.

Thursday's dollar experienced its worst day since March 2009

Stock market short positions are the largest since the 2020 covid-driven rally.

The fixed income market and in particular the US2yr and US10 yr eased strongly in the face of the inflation data, highlighting a sharp drop in the MOVE (the equivalent of the fixed income VIX).

In our opinion, it is too early to assess and celebrate a drop in inflationary pressures, but the market has been anxiously looking for a positive data for weeks to start a rally to relieve all the prevailing bearish pressure. We continue to see a market that reacts to short-term stimulus and wants to ignore the macroeconomic situation we are going to experience in 2023. A PIVOT from the fed may bring short-term joy, but it is an unmistakable sign of new problems and an inevitable entry into recession.

Macro data and economic activity indicators remain in line, especially in the old continent.

A U.S. survey has shown that 49% of restaurants and 40% of small businesses were unable to pay their rent last October. The damage that inflationary pressures are doing to the real economy is undeniable and spans the entire market, from small businesses to large corporations.

We now find ourselves in the following situation:

Two consecutive quarters of negative GDP.

2. Lowest earnings growth since the third quarter of 2020.

3. Real estate market with the fastest fall since 2011

4. 2 Trillion $ in crypto losses and collapse of FTX

However, the Fed continues to insist that a "soft landing" is possible. We certainly severely doubt these claims and all indications are that the Fed has completely lost control.

Cryptoassets

This week we have experienced an exceptional situation in the crypto ecosystem.

A few days ago, the soundness of the financial position of FTX, the world's third largest crypto exchange, was called into question when the balance sheet of Alameda Research, a hedge fund linked to FTX and owned by the exchange's CEO, came to light and seemed to indicate financial problems. Soon after, what everyone expected was confirmed: the value of the assets did not match the value of the liabilities, something that caused panic in the market.

Investor confidence plummeted when on Sunday 06/11/22 Binance CEO Changpeng Zhao posted: "we have decided to liquidate any remaining FTT on our books." explaining that they were set to liquidate their entire position of over 2.1 billion in the FTX token called FTT. It was a full-blown liquidity crunch and the FTX token fell by more than 75% on the day, generating a great deal of distrust and exerting great selling pressure on the entire market after the price of the token dropped from $25 to $4. This created severe problems for FTX and Alameda Research, who controlled almost 80% of the supply of this token and who had used it as collateral for loans. With the fall in the price of the token, the gap between their assets and liabilities increased to eight billion dollars.

Binance, the largest exchange in the sector, announced that they had signed a letter of intent with FTX to buy the exchange and thus rescue it, but a few hours later they announced that they were withdrawing the offer because the hole in the balance sheet was larger than expected. Currently, FTX has entered bankruptcy, filing for Chapter 11 with more than 135 related companies.

All this has generated a real earthquake in the crypto ecosystem, the contagion effect is inevitable due to the close relationships between the main players. Over the coming weeks we will learn about the collateral damage of this event, which has already been defined as the Lehman of cryptos. What has happened is a further demonstration of the superiority of decentralized finance over the traditional financial system. Centralized exchanges, such as FTX, Celsius, Voyager, etc. operate exactly like a traditional financial institution, but with less regulation. Despite the impact this has had on the market, all decentralized exchanges, decentralized lending platforms and other decentralized finance protocols have continued to operate normally and without any disruption. Everything that the FTX board has done wrong would have been impossible to do in a decentralized finance protocol. We are seeing how many users are moving their funds from exchanges to their own wallets, which is what blockchain and crypto were invented for; it is where the future of this technology lies, which will come out of this incident stronger.

In this week's newsletter we will go longer than usual, analyzing not only the price action but delving in more detail into the information obtained from the options market and on chain metrics. The crypto ecosystem has experienced an earthquake of the highest possible magnitude on the Richter scale, we remain defensively biased as last week but attentive to possibilities, which usually appear in moments of climax and generalized panic that have more emotional than rational components.

Bitcoin

As we indicated in the previous newsletter, a failure of continuation of the blue minor structure and the inability to consolidate above 20500 was going to put the market in trouble and so it was. The dynamite was in place, the only thing missing was to light the fuse, which came from the fall of FTX-Alameda and the storm in the rest of the ecosystem.

The June lows have been swept away with sharp percentage declines during the past week, however it is important to emphasize the information provided by the options market as extreme readings are a prelude to reversal movements of the prevailing selling pressure.

A move to the upside to test the main vpoc of 19160 is not farfetched given the oversold situation and climax of many metrics. For this we want to see the market in the short term consolidate above the vpoc of this value area (16875). If buyers manage to win this battle, it would open the door to a short squeeze that could lead the price to re-enter the main range shown above and attempt an attack on the main Vpoc (19160).

The order book remains heavily protected on the downside on both Binance and Coinbase, with the path fairly clear to the main vpoc of 19160.

The skew, which measures the difference between the IV (implied volatility) of OTM puts and the IV of OTM calls, shows extreme readings reminiscent of the end of the May and June declines.

The IV of the ATM options also gives us climax readings.

The volume-weighted funding rate shows the true selling panic in the derivatives markets, as sellers are paying buyers funding rates typical of a market in climax; in fact, such rates have not been seen this year.

Last week we already anticipated that the balance of Bitcoins on the exchanges was rising sharply, which could be interpreted as a potential selling pressure in anticipation of events or even a preparation for a major sell off, coincidence? obviously not.

After last week's sell-off, we are now seeing the other side of the coin, with significant outflows of Bitcoins from exchanges, although we must be aware that a large part of these outflows are due to the generalized CEX panic. However, we do not doubt that some entities consider this Bitcoin price attractive for positioning. From Minnesota expert Warren Buffet, we extract the following sentence:

"Be Fearful When Others Are Greedy and Greedy When Others Are Fearful".

The percentage of supply in profit is at levels similar to the March 2020 capitulation (covid market shock).

The price of Bitcoin is touching the lower band of the average production cost, the market has to consolidate a floor at these levels so that the economic incentive to mine bitcoin remains alive and does not jeopardize the sustainability of the network.

The miners, as expected, under serious pressure this week distributed 8000 btc, about 9.5% of their balance sheet.

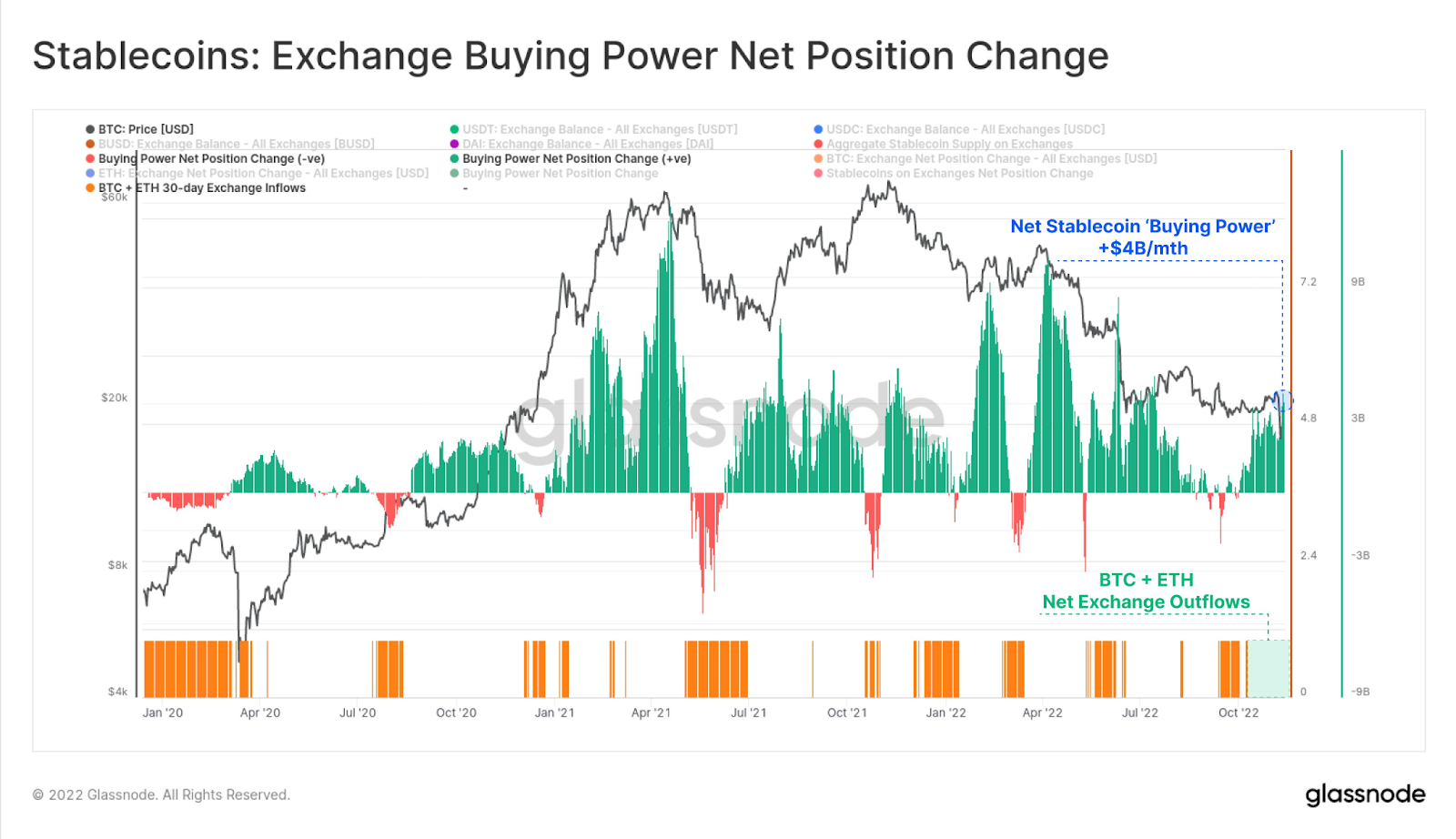

The stablecoin inflows to the exchanges during the week have experienced a remarkable increase, about 1.04 Billion entered the exchanges after the collapse of FTX.

Total stablecoin reserves on the exchanges have reached a new all time high, 41.18 Billion, highlighting the increased dominance of BUSD, in the face of some stablecoin depeg problems during the storm.

The exit of BTC and ETH from exchanges along with the entry of stablecoin into exchanges has led to a net increase in stablecoin "buying power" of about 4B/mth

Ethereum

The market overlap in the $1500-1600 area was not a good prelude to buying strength. The FTX event has caused the market to go after the lower buying control with wild verticality. However, that buying control ($1100) is holding. Ethereum must regain the Vpoc of the volume composite (1325) to unwind this selling momentum. The price control levels are clear and this gives us as it could not be otherwise, the volume per level (volume profile).

Classic markets

The market after the failure of the bullish continuation of the main structure returned to the inside of the range, to the value. Delicate moment for buyers, as it is the last trench of demand control.

The inflation data, 0.3% less than expected, was good enough for the market to trigger a bullish explosion and put the price above even the previous bullish continuation failure.

During this week the market should validate the bullish move with an effective imbalance as marked in the chart. The auction that has left the market with this move is disastrous and the flow of options so focused on the short term is still predominant, which is not positive at all.

The 390 level of the SPY is key, if the market truly wants to continue higher, the breakout and test above that level must be confirmed. It is clearly the line in the sand for all risk assets currently.

If we analyze the price of the SP500 with respect to the liquidity present in the system, we can see that the market is certainly overvalued.

Net Liquidity is the portion of liquidity available to circulate freely within the economy, resulting from the Fed's Balance Sheet expansion through Quantitative Easing (QE).

Net Liquidity = Tot Balance Sheet - (TGA + RRP)

NetLiquidity=TotBalanceSheet-(TGA+RRP)

The liquidity inside the Treasury General Account (TGA) and the Reverse Repo Facility (RRP) is subtracted from the Total Assets in the Federal Reserve's balance sheet because effectively removed from circulation.

.png)