.png)

Summary

The big week that will inexorably mark the future of the markets has arrived: US CPI. FED meeting (FOMC rate decision), Boe, the ratio decision by ECB, US retail sales, 90 billion in auctions of US bills and bonds and OPEX (US options maturity with 3.7 trillion notional). We have already seen on previous occasions that the US inflation data is the most important thing at the moment for the market, a market that lives from day to day, ignoring the complicated macroeconomic situation that we are going to face in 2023 and that seems to only move by cannon fire resulting from data and statements.

The crypto ecosystem is still mired in the collateral effects of the FTX-Alameda storm, some doubts are starting to be heard about Binance's proof of reserves along with apparent depeg of USDD, Tron Network's algorithmic stablecoin. Now more than ever: "not your keys not your coins".

Macro analysis

Relevant data for this week:

Tuesday: Inflation Germany, US CPI

Wednesday: Fed, rate decision, Powell press conference.

Thursday: BoE and ECB rate decision, US retail sales.

Friday: Eurozone Inflation

In the newsletters of the last two weeks, we focused on analyzing various economic activity indicators, which showed contractionary and certainly very worrying readings in the profit forecasts of companies for 2023. It is important to be clear about the context in which we are moving in order not to enter into the short-termist game in which the market is immersed. This past week has been very anodyne in terms of data, we can highlight the "blackout period" of some members of the FED, the only data of relevance which has been the US PPI.

PPI 0.3% M/M; Exp. 0.2%; Last 0.2%.

PPI 7.4% Y/Y; Exp. 7.2%; Last 8.0%.

PPI Core 0.4% M/M; Exp. 0.2%; Last 0.0%.

PPI Core 6.2% Y/Y; Exp. 5.9%; Last 6.7%.

Winter has arrived and the structural energy problem is far from being solved in the short term. Europe and the UK will have to deal with the problem of energy shortages and overpriced raw materials.

Gas demand in Europe has fallen by -25% compared to the average of the last 5 years, and we certainly doubt that this is the result of the savings and containment measures implemented within the EU, but rather a drastic drop in industrial and economic activity.

LNG import prices (maritime transport) are at record highs and are predicted to remain so during the winter. The spread between JMK (Asian benchmark) and the TTF (European benchmark) remains in favor of the EU, gas is arriving, but at astronomical prices. The TTF exploded again this morning and prices for hours 17-18 in Great Britain reached 2000 GBP/Mwh, insane.

As we have already said, winter has already arrived and these are the first warnings regarding the weak energy situation Europe is facing. France already seems to be talking openly about power cuts and how they will be carried out by region, from 8.00am to 13.00 pm and from 18.00pm to 20.00pm only with 3 days notice.

China's November trade figures (trade balance) once again came in well below expectations. November exports were $296 billion, down 8.7% from a year earlier, while imports were $226 billion, down 10.6%.

The market is waiting for China's major "re-opening" with a relaxation of the strict zero covid measures. The Asian giant's top health authority said over the weekend that the risks associated with Omicron are similar to those of traditional influenza.

At the same time Beijing has ordered major market participants (mostly government agencies) to buy bonds to alleviate the panic selling of the last few weeks, one could say that China is quietly launching its own QE.

The Fed has already stated that it is concerned about an overheated labor market that continues to provide inflationary pressures hand-in-hand with wages. The huge divergence between wage growth for job changers and job stayers is worrisome because it indicates an imbalance in the labor market (2 charts). Demand for labor remains extreme, suggesting that the Fed may need to tighten policy more than expected.

Next week's newsletter will be in line with this week's intensity. The market awaits with great anticipation the November inflation data and Powell's reaction afterwards. The inversion of the US 2yr-10yr curve has reached -0.837%, one has to go back to the 1980s to find similar readings. It seems that the fixed income market is no longer thinking about inflation and pivots, but is starting to seriously discount a recession scenario.

The Federal Reserve reduces its balance sheet and therefore the liquidity in the system and the result is the following, a picture is worth a thousand words

Cryptos: spot, derivatives and on Chain metrics

Little change over the past week, we remain above the vpoc of $16600, although with signs of weak demand for continuations to the upside. This week is key for all markets and the crypto ecosystem is not on the sidelines. Waiting for the inflation data and Powell above the $16600 control level is certainly much better than below it.

Bitcoin

06/12/22

12/12/2022

As long as the market manages to stay above the vpoc of $16600, the bias remains long. This week is expected to be particularly volatile, it is important to be clear about which levels the bulls must defend and which battles the bears must conquer. Any break and consolidation below the control level mentioned above, would cause an immediate change of bias, do not forget that there are many open fronts (macro, Fed, FTX-Alameda contagion) that can have a high impact on the price.

From the point of view of price dynamics, the sequence of declining highs and lows has been broken, entering a bullish dynamic, of rising highs and rising lows. However, in the final part we are starting to see a weakening of demand, which is not able to push the price beyond $17400. The market awaits the events of the last relevant week of the year.

The order book is still strongly protected on the lower side, and with some relevant movements on the upper side, the upper walls of limited returns, specifically in the area of $17500, $17800 and the main vpoc of $19000. Below, close to the current price, some support, albeit minor. The market is very tight ahead of this week's events. These events will undoubtedly be the catalyst for the next major move.

The skew, which measures the difference between the IV (implied volatility) of OTM puts and the IV of OTM calls, has seen a very noticeable easing over the past two weeks. The panic and climax readings are behind us, the market seems to have shaken off the prevailing fear of recent weeks and has entered a period of calm after the storm.

skew 06/12/22

skew 12/12/22

The at-the-money volatility curve clearly shows a noticeable jump heading into this Friday's 12/16/2022 expiration, which picks up everything that is coming up this week,

This "fear" priced into the market is also reflected in the spread between RV (realized vol) and IV (implied vol), the readings are similar to previous high market impact events, November 10, US inflation November and November 22, Powell's press conference.

On December 30, we face the last important expiration of the year in Bitcoin options on Deribit (centralized exchange that gathers most of the volume traded in options). The "max pain" (level where most options end up with no intrinsic value, i.e. worth zero) is above $19,000. Undoubtedly, market makers are the first ones interested in the price reaching that level for this great expiration.

In terms of delta (market aggression) on Binance perpetual futures it seems that the strong selling pressure of the FTX event. The market in terms of buying and selling pressure to market remains fairly neutral without giving us any major clues. The price dynamics discussed above already clearly indicate this issue.

Volume-weighted funding provides us with online information. The selling panic resulting from the FTX event gave us insane numbers in terms of shorts paying longs. In recent weeks, total ambiguity, the futures market has no clear bias.

We continue to observe outflows of Bitcoins from exchanges, such dynamics can be considered as moderately bullish, it is correct to think that many market participants withdraw their Bitcoins from exchanges and keep them in cold wallets.

The increase of Bitcoins on the exchanges from the end of August to the beginning of November was clearly a reason for caution, and even more so after observing the failed demand dynamics. It is not unreasonable to think of a preparation prior to the FTX event, as of today, the outlook in terms of Bitcoin balance on the exchanges has nothing to do with the current situation.

Ethereum

Remarkably unchanged from last week, the market remains above the $1225 control level. If the market really wants to reverse the prevailing situation, the value area marked in white has to show clear signs of re-accumulation. After consolidating the $1225 level as it is doing now, the market must look for the top of the range to subsequently try to unbalance the whole commented structure. On the other hand, a breakout and test inside at the 1225$ vpoc would nullify any bullish approach in the short term.

06/12/22

12/12/22

Classic markets

The market after touching the gamma call wall at 4100, leaving a bullish imbalance failure above it, has gone through the entire value area with a lot of verticality, this in the Wyckoff methodology is known as "sow" (sign of weakness). The market is waiting on the edge of the precipice for all the events of this week. It is worth remembering that this entire upper value area is supported by a spike without trading and market auction resulting from the inflation data for the month of November.

SP500 Futures 06/12/22

SP500 Futures 12/12/22

The big question now is the following: re-accumulation at the bottom of the range, to save the move or redistribution to look for lower areas of interest such as the HVN (high volume node) of 3800 points? It is certainly worrying that the market validates scenarios based on one-off events such as data or press conferences. Lately everything is quite similar to red and black roulette and for us it is a clear warning that the markets are not working organically.

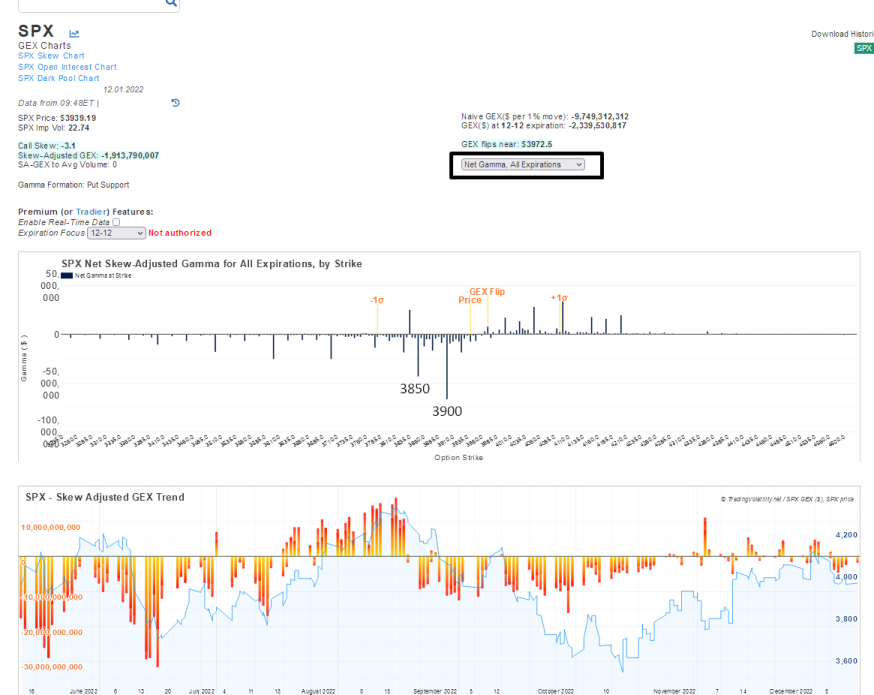

Gamma profile 06/12/22

Gamma profile 12/12/22

The market's gamma profile clearly reflects the market's perceived fear of this key week, which is also an options expiration week (OPEX). The strike with the highest gamma notional is 3900, followed by 3800. A market in a negative gamma regime implies that the market maker hedges in favor of the market movement, accelerating the movements in both directions. The Gex Flip, zero gamma level is always a turning point in the market and in this case it is the level that clearly has to conquer the demand.

The gamma curve (in this case of the SPY) has a steep negative slope between 395-375 points, if the data and Powell disappoint and make the pivot narrative unsustainable again, the market could accelerate very quickly to the downside in this price range as market makers would have to aggressively hedge by selling spot / futures.

Conversely, if the pivot narrative finds support again, all this bearish positioning would again be fuel for a big short squeeze. Theta (time in option Greeks) and vanna (changes in vega, IV of options) strongly erode the value of option premiums and even more so with option expiration so close.

The VIX seems to have started to wake up, after touching again the 20-18 zone. The test to that zone has previously been the signal of the completion of the previous bullish impulses as we mark in the following chart.

Finally, some metrics of the equity markets, which in some cases we will keep in our historical archive.

Retail investors are far from having capitulated this year, their exposure to equities remains very high. Holdeo is not only part of the crypto culture.

Passive management in the USA has clearly overtaken active management since 2020, already holding a 56% share according to Goldman Sachs. Globally, the overtaking is imminent.

In a passively managed vehicle, stocks are simply put into an ETF and bought that way, they may be overvalued and no one will check anything to find out if the prices are in line with reality. This is a far cry from the idea that the market facilitates the efficient allocation of capital. Passive management strategies in turn allow short squeeze events to occur with greater frequency and greater severity. In the worst case, an instantaneous forced liquidation of positions could lead to strong distortions in asset prices by draining liquidity very abruptly.

.png)